Shake Hands and Get Five Fingers Back

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

December 2, 2023By avoiding companies failing our strict Integrity Screen, we manage to navigate the risks of investing in India and enhance sustainable long-term returns. Keeping governance and transparency as priorities has proven crucial, even as some high-flying stocks periodically try to test our resolve.

In 1996, stung by experience, we initiated what we called the ‘Integrity Screen’ as a filter for our investments.

A conscious decision to avoid investing in companies with suspect corporate governance. No matter how large they were. No matter what products and services they built. No matter how much weight they had in the index. No matter how much important they were.

We called it “shake the hands and count your fingers back” – a test of treatment of minority shareholders.

If they did not pass this test, we will avoid investing in those names.

If they did not pass this test, we will avoid investing in those names.

However, Investors, especially foreign investors, increase their risk profile when they invest in Indian equities.

This risk then is not just standard deviation. The risks do not always get captured by a mathematical or a statistical number.

Quantum’s research and investment process is built on the principles of avoiding and managing three inherent risks in India : a) Liquidity – not only of the underlying for entry and exit; but also of the scalability of the strategy; b) Governance – avoiding India’s myriad crony capitalists and managing reputation and headline risk for our investors and c) Valuation – buying India’s ‘growth’ with margin of safety

Our job as an investment management firm is to assess, manage and control that risk. Not enhance it.

In this thematic, we look at the risks from governance. And detail what we mean when we say – ‘Shake Hands and invest only with those managements where you get your five fingers back.

In a country like India, where the representatives of Indian industry are fondly referred to as “corporate honchos”, “leading industrialists”, “captains of industry”, “the face of new India”, or just plain “filthy rich” – you inherently know that you need to be very careful while investing.

With some of them, forget fingers you might lose your ‘entire arm and a leg’.

Investors who do not care about governance , reputation and headline risks, can of course ‘roll the dice’ by investing in the Indian indices and managers and brave their share of Enron, Worldcom, Yukos, Wirecards.. that exist in India.

For those who care, it might be worthwhile to understand how we think of Indian companies, their businesses and the integrity of the managements.

We Avoid or We Engage. We talk about the integrity screen and the engagements with a few examples. It shows how we have learnt and refined the integrity screen over the years and also detail some of our engagements with corporates on their behavior and treatment of minority investors. Some with success (for eg- our efforts and engagements with ICICI Bank ) and some with failure leading us to exit those companies (eg; Ranbaxy, L&T).

In this piece, we look at one another way of trying to figure out suspect managements.

We believe that market prices also tell you some stories. Stories, not only about, the businesses and the opportunity but also about the character of the management. It can also tell you how close or dependent the company is to government policy action and/or favors.

Difference in governance is visible in market valuation for instance. In some cases, the market loves a particular management style in bull markets, but when the tide turns, as Warren Buffet reminded us ‘ ….you learn who has been swimming naked’.

We also see a clear pattern of market reaction on key events and dates. Scroll through the slides below to see ‘Governance in Action’ – how market price movements reflects markets reading of different managements. And why sometimes it is not that hard to avoid suspect managements.

What is hard is to have the courage to stay away from them and deal with likely periodic underperformances that you suffer.

This is why it is important to build these kinds of ‘integrity screen’ into the investment process as a rule and not as an exception.

We use 8 event dates to show how select stocks responded to the events.

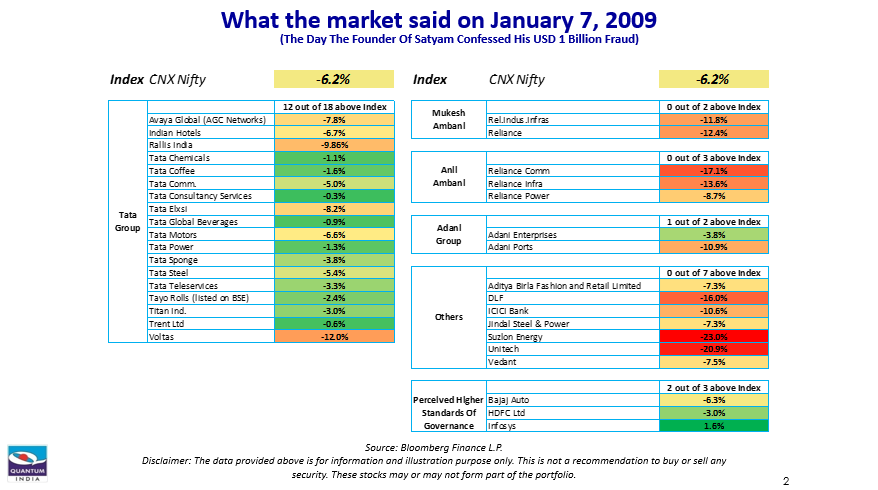

- January 7, 2009 – The day the Satyam Computers Founder wrote to the stock exchanges admitting the fraud stating, “it was like riding a tiger not knowing how to get off without being eaten” – markets were sort of telling us, who they think is the next Satyam

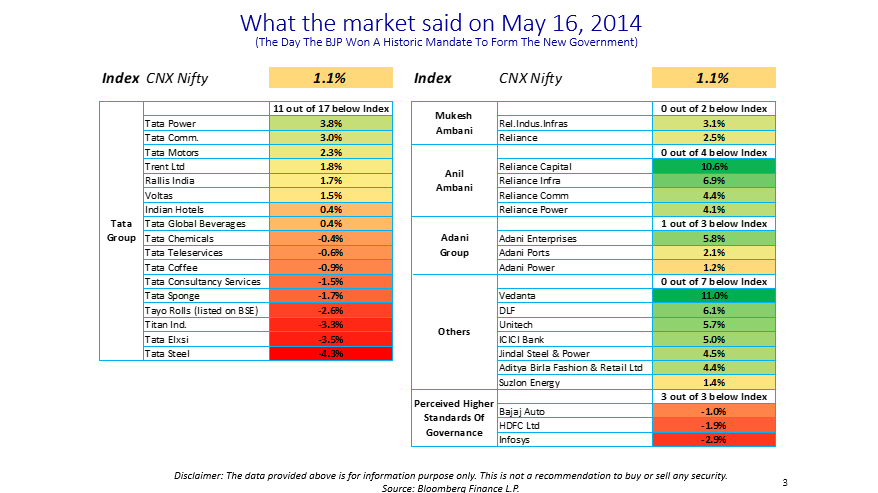

- May 16, 2014 – the Day BJP and Modi won the general elections – market perceived him to be ‘pro-capitalists’ and stocks of crony capitalists did well

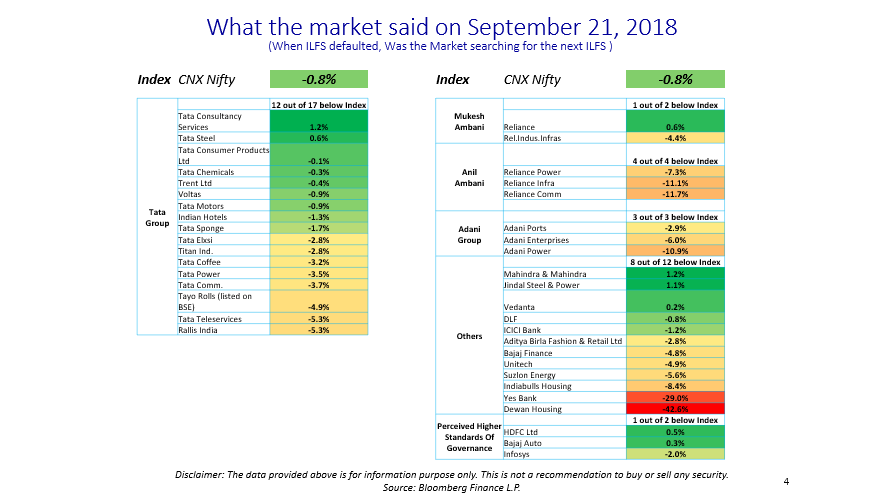

- September 21, 2018 – The day when ILFS defaulted and market price response suggested they were questioning the balance sheets of some other financiers

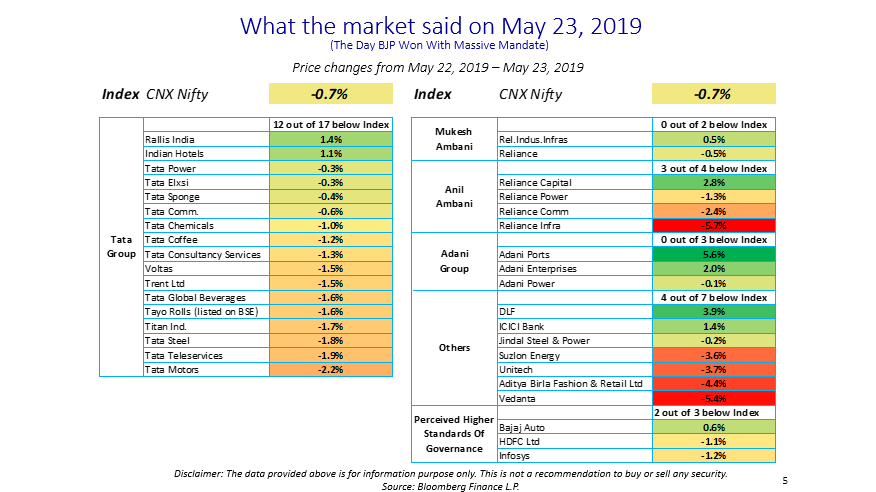

- May 23, 2019 – PM Modi re-election in 2019 – a stronger mandate.

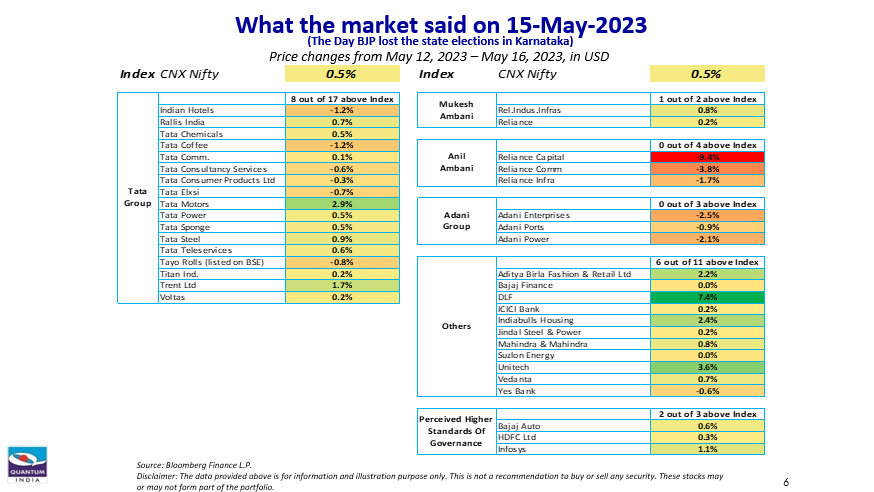

- May 2023 – Loss in Karnataka elections for the BJP – an indication that sectors and businesses linked to government policy and to the party may struggle

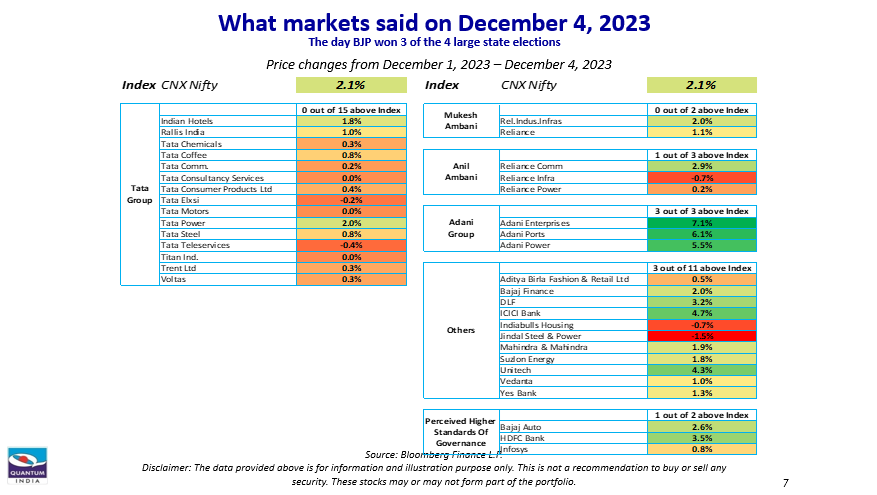

- Dec 4, 2023 – Results of recent state elections with a resounding win for BJP.

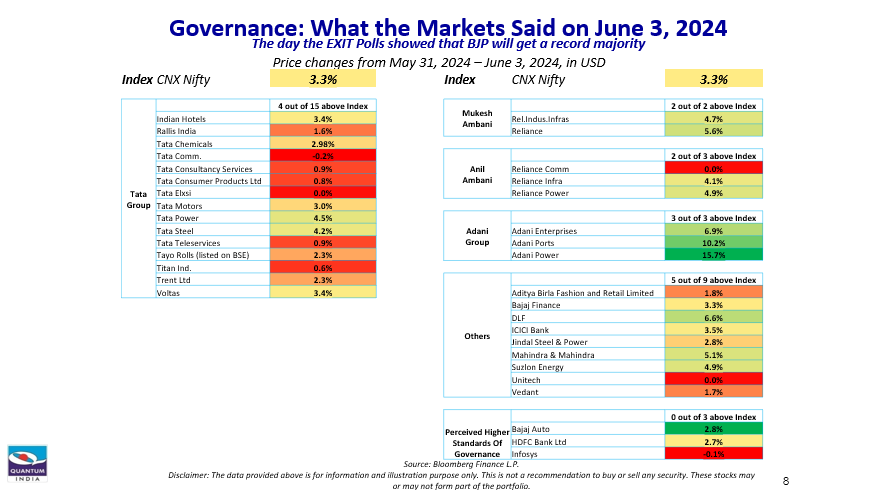

- June 3, 2024 – The day the EXIT Polls showed that BJP will get a record majority

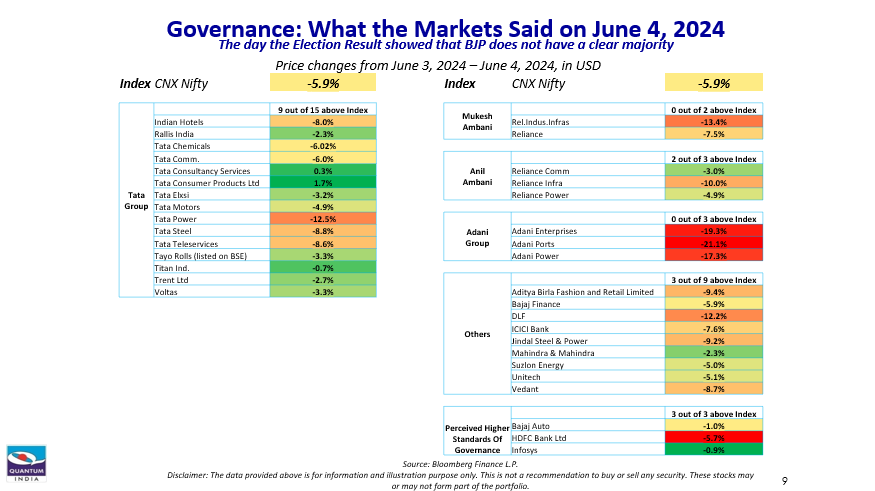

- June 4, 2024 – The day the Election Result showed that BJP does not have a clear majority

Governance in Action

A look at share price movements on key event days to understand what market tells you about integrity of managements and its link to government and crony capitalism

Chart showing stock price reactions of selected companies after the Satyam fraud announcement in January 2009, highlighting sharp declines.

Source:

Chart illustrating stock market movements of selected companies following the 2014 Indian general election results, showing positive momentum.

Source:

Chart showing stock price responses of financial companies after the ILFS default in September 2018, reflecting declines due to liquidity stress.

Source:

Chart depicting market reaction of selected stocks after the 2019 Indian general election results, indicating strong positive trends.

Source:

Chart showing stock performance of selected companies after BJP's Karnataka election loss in May 2023, with mixed reactions.

Source:

Chart illustrating market reaction of selected stocks after BJP's state election wins in December 2023, reflecting positive sentiment.

Source:

Chart showing stock market reaction on 3rd June 2024 when exit polls indicated a clear BJP majority, with upward movement.

Source:

Chart showing stock market reaction on 4th June 2024 when election results showed no clear majority, with noticeable declines.

Source:

Related Post

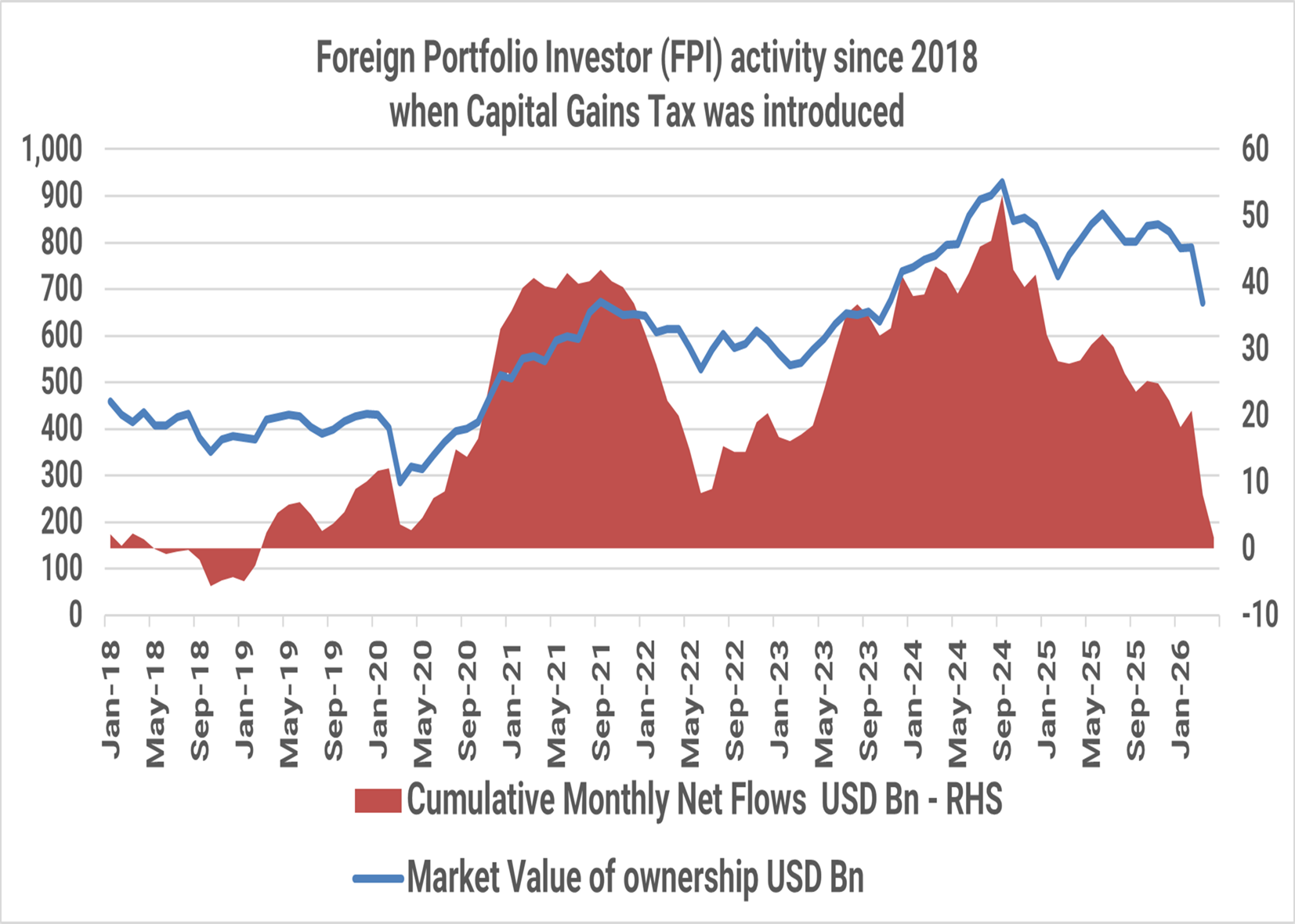

India: T I N A to A N T I

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

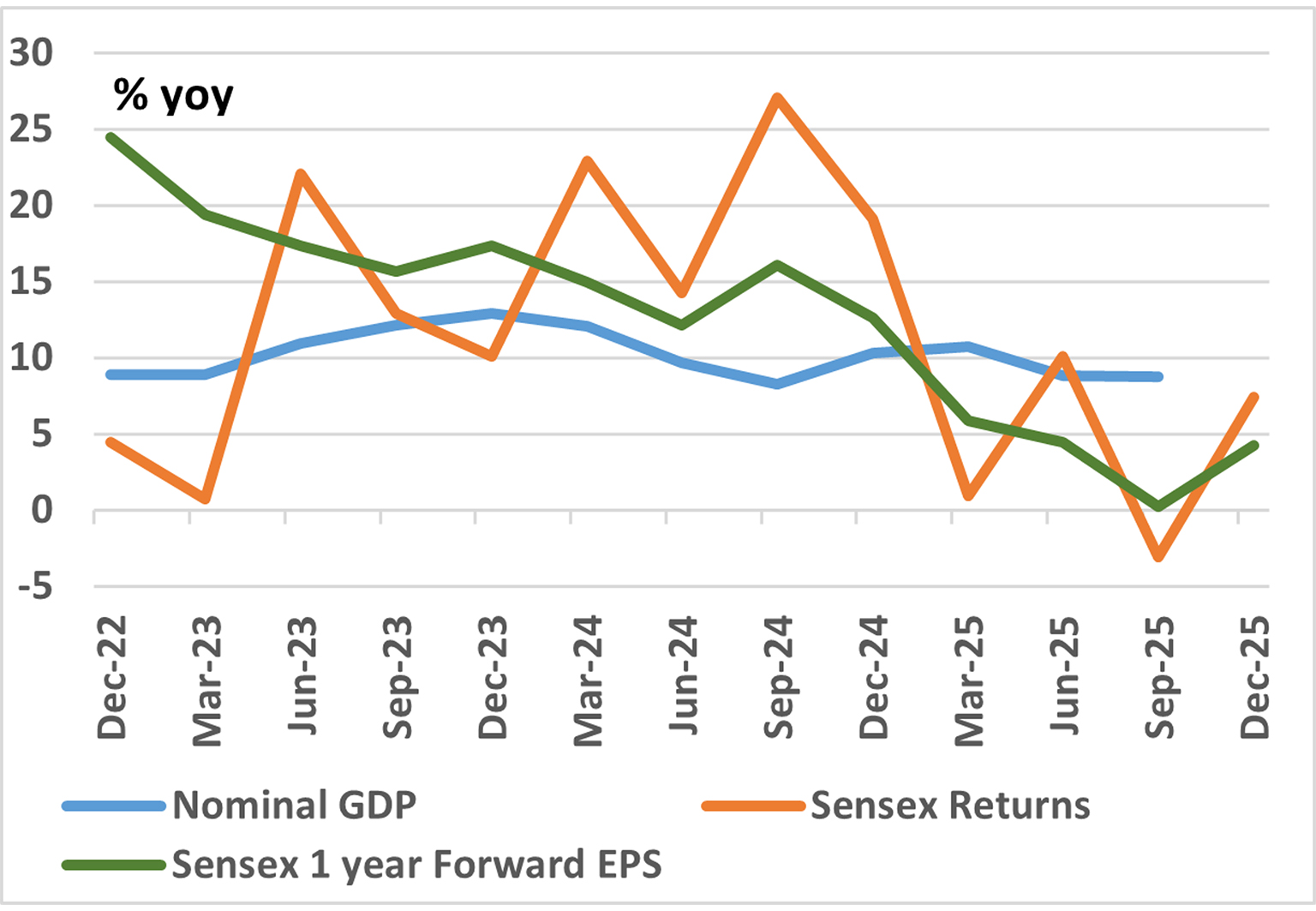

India Investing: From a complicated 2025 to a Simpler 2026?

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

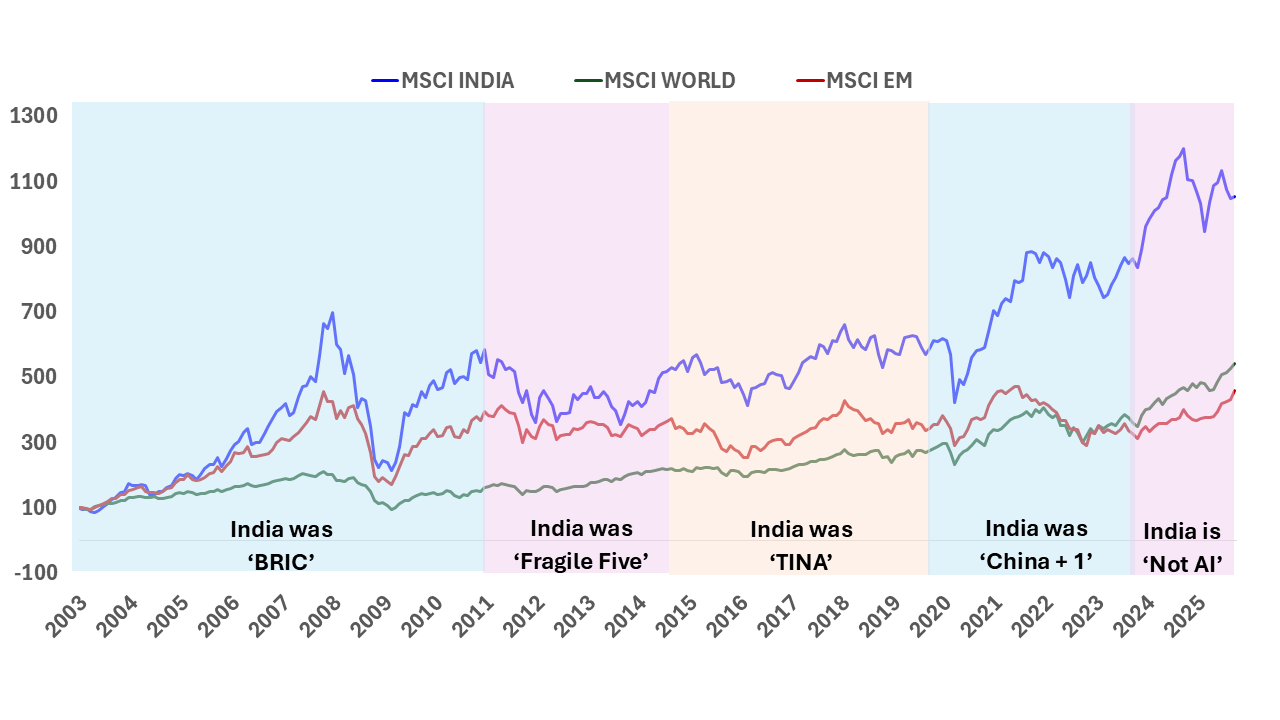

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.