India - FDI in Retail - A Silver Bullet?

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

Nov 5, 2012The Indian government thinks it has a silver bullet in its new FDI retail policy - to solve the country's macro challenges.

On the domestic front, the Right to Information Act has brought a series of questionable government-corporate deals out into the open. For the first time in India's economic history, members of the ruling federal and state governments and its decision-making Cabinet have been sent to jail (along with CEOs of Indian companies) as the prosecutors prepare cases of corruption.

Depending on whose opinions you rely on, this is being referred to as a witch-hunt or a cleansing. The self-styled chieftains of India's corporate class are upset at the “policy paralysis”. They grumble that approvals are not being granted for a range of projects. The bureaucrats and politicians are too scared to take decisions that may put them in trouble. Furthermore, the “progress of files” is being hampered by environmental and tribal protection laws.

There is certainly a slowdown in actual investment. If this carries on for a few more quarters, it could result in the wide-eyed, 8% rate of growth in GDP being an illusion. Foreign investors are fearful of such an eventuality - they have been betting on an 8% growth in GDP. A “risk-off” mentality makes them net sellers of Indian stocks (Table 4).

Looking for some silver bullets

Our view on this is, well, different. A 7% rate of growth in GDP, in our humble opinion, with less corruption money flowing through the system is far better than a torrid 8% or 9% rate of growth in GDP where grease money not only oils the wheels but also makes sure the gravy train is loaded in favour of a few.

Meanwhile, bombarded by criticisms of policy paralysis, the government fired two silver bullets: allowing foreign capital to invest in Indian fixed income products (to fund infrastructure spend) and a new FDI policy for retail.

But the attempt by the Indian government to show its strength by announcing the guidelines for full-fledged foreign investment in India's USD 450 billion retail market has been embarrassing. While the final fate of this “big reform” is not known, suffice it to say that - even if it passes through a stubborn Opposition - it is merely an enabler. Every state government has the option of accepting this new FDI policy, rejecting it, or modifying it to suit their needs.

The argument for allowing the WalMarts of the world is that it will improve logistics, reduce the costs of production (since big-box retail weakens the negotiation power of suppliers), and create more jobs as the supply chain logistics and stores get built out. Overall, the economy will benefit as costs of production and inflation are reduced. It will be a win-win. But critics warn that these were probably the same arguments used by the auto (and other) manufacturers in the US as they lobbied their way into free-trade agreements and lower tariffs. And over time the impact has been numbing.

The US has lost 6 million manufacturing jobs between 1978 and 2007. And it has added 50 million service jobs - amongst them the minimum wage jobs of flipping hamburgers and pushing crates in Wal-Mart stores. In 2005, salaries in manufacturing jobs in the US paid 23% more than salaries in services. Sure, consumers in the US are a lot “better off” with a myriad of choices - and USD 11 trillion of debt to show for it! While there is the “numbers argument” for a more open economy, countries may be at various stages in their development. And, given where a country is, the policies it adopts may differ.

BRIC is built on an assumption

For example, the conclusion from Goldman's BRIC report was that India would reap a “demographic dividend”. The economists at Goldman forgot to dig deeper and see how jobs would be created for those additional 100 million youth by 2025. When asked, they responded that their models assumed the government would put in place such sensible policies! If only such a government existed - anywhere in the world. An assumption in an xl sheet is a wonderful solution to the real world dilemma on how 27,000 new jobs need to be created every day for 3,650 days to absorb the young productively! (As readers know, this is the only risk we see in India: 100 million youth hanging around urban street corners with little to do is a social time-bomb).

But we live with real-life policy choices and not in assumed xl sheets. At one extreme, India can manufacture spades and give it to the 100 million to build roads and bridges. At another extreme, India can buy out all the capacity of heavy equipment manufacturers like Caterpillar to build those badly needed roads. The policy path chosen will lead to either, higher employment (and roads being built at a slow pace) or to lower employment (and roads being built at a faster pace).

With 9 million retail touch points across India, the fears of Wal-Mart dominance are limited. Data suggests that over 90% of the retail “stores” in India are less than 500 square feet. Given the diffused nature of the retail business, while some city-centric, relatively larger, retail stores may be under immediate threat, most would not be. One would not expect WalMart to open a store in each of India's 640 districts - in fact, the proposed rules would only allow foreign retail in 53 cities with a population of over 1 million. These 53 cities have an estimated 15 million employed in the retail business.

Proponents of FDI in retail argue that McDonald's has not displaced the local Indian eateries. And Hollywood has not displaced Bollywood. Farmers, apparently, are keen to see big box retail in India as they believe it will allow them to sell to one large buyer at higher prices, without middlemen. That hope may be belied as a large buyer eventually strangles pricing power of the seller. Those dealing with the monopsony of WalMart know the feeling.

But couldn't the same objectives of bringing costs down, improving the price received by farmers, and giving consumers more choices be brought about by improving the supply-side chain and cold storage issues - without touching the issue of where these items are sold? Over 30% of Indian agricultural production rots in the farms. A myriad of sellers linked to a myriad of buyers in an efficient network would remove pricing power at any end - and create some of those 100 million new jobs. But improving the intermediaries, unfortunately, requires hard work. And everyone wants a silver bullet - the Indian government thinks it has one in the new FDI retail policy.

Related Post

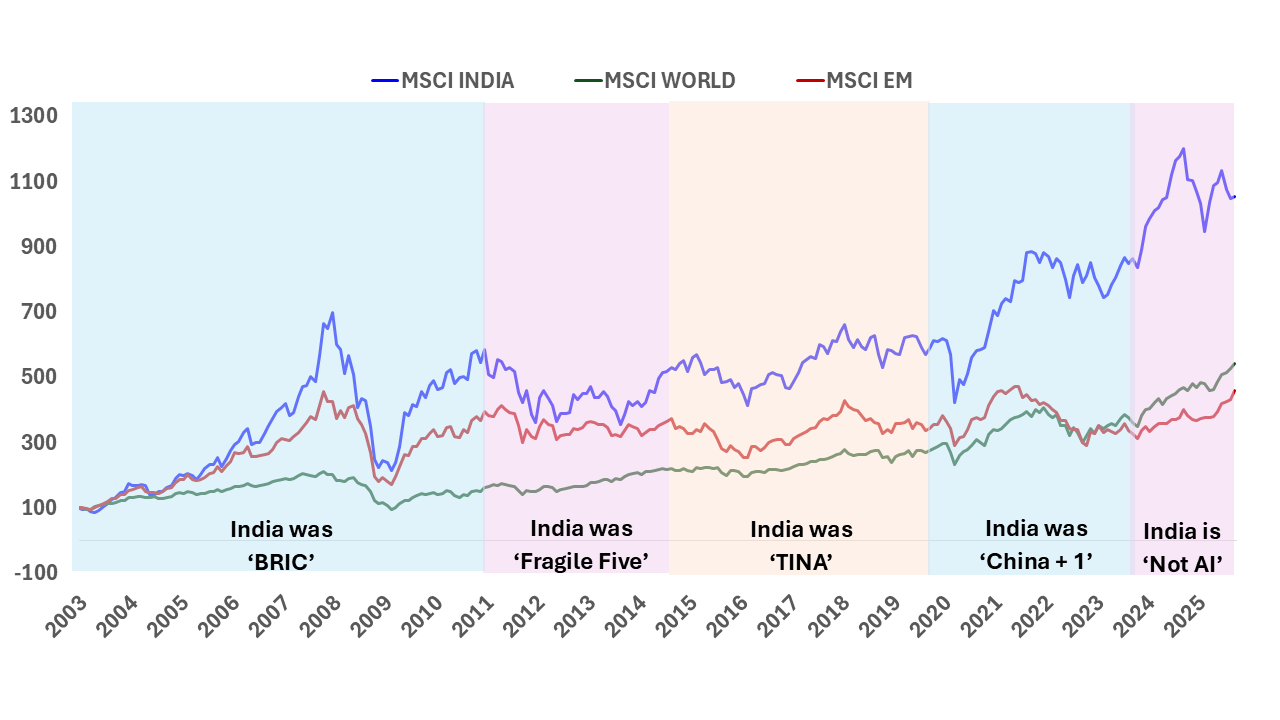

India: T I N A to A N T I

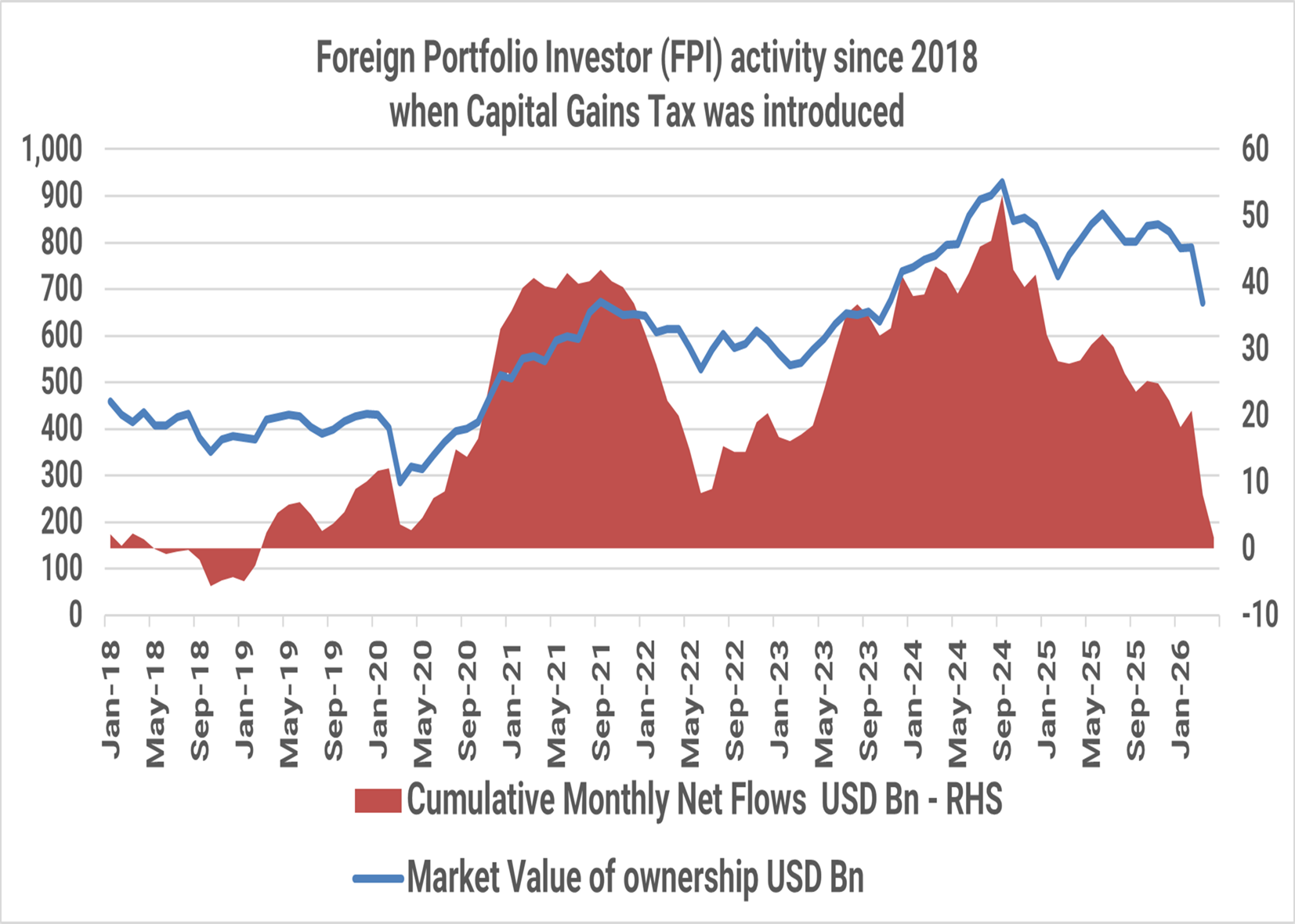

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.