.webp)

Great Expectations and a New Reality

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

June 2, 2014Market expectations for the new government offers new realities and challenges to value investors.

From a stock market perspective, the Modi fever continues unabated. Ever since the historic win in the recent elections, the markets have valiantly reached successive peaks driven less by factual actions and more by Great Expectations.

An online survey (Table) suggests that 50.04%, a tantalising slim majority but a majority nonetheless, expect Prime Minister Modi's economic policies to result in India achieving >8% real rate of growth in GDP over the next 4 years. Given that India is at a sub-5% level of growth - and the global environment is what it is - that is indeed a lofty (but not impossible) expectation.

Table: What will the GDP growth rate be during 5 years of Modi’s rule?

| Range of rate of growth in GDP | Percentage of votes |

|---|---|

| Less than 6% | 8.88% |

| 6% to 8% | 41.09% |

| 8% to 10% | 38.74% |

| Above 10% | 11.30% |

A new reality

These are certainly testing times for a disciplined value manager. On one hand there is the reality of a poor operating environment in which the companies in the portfolio are currently operating in. On the other there is the expectation that this operating environment will improve dramatically with - as the covers of The Economist, a magazine, indicate - some pretty strong expectations.

And while all equity investors by definition have optimistic expectations, our challenge is that the prevailing expectations of Ram Rajya (a goldilocks sort of environment sprinkled with some spirituality) is something we have not been able to digest as an “expected given”.

Needless to say, there is the not-so-subtle question of what sort of managements are likely to do well in this new Ram Rajya: will it be an India powered by meritocracy or will it be an India powered by the hypocrisy of crony capitalism? The kind we had under the mis-rule of an intellectually bankrupt Congress.

As investment managers with an “integrity screen”, that matters a lot. If the operating environment favours the well-connected as opposed to the entrepreneurial, it could lead to lower cash levels (we may be buying the declining shares of the entrepreneurial) but with a risk of “under-performance”

Related Post

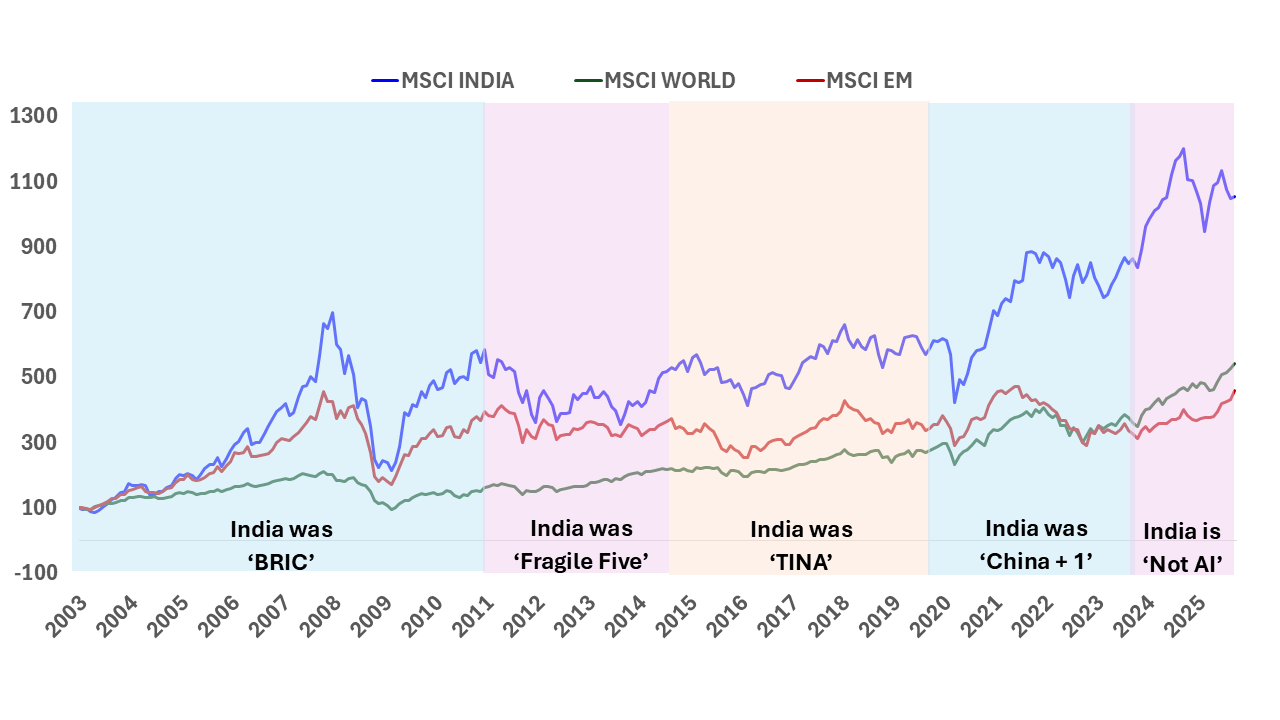

India: T I N A to A N T I

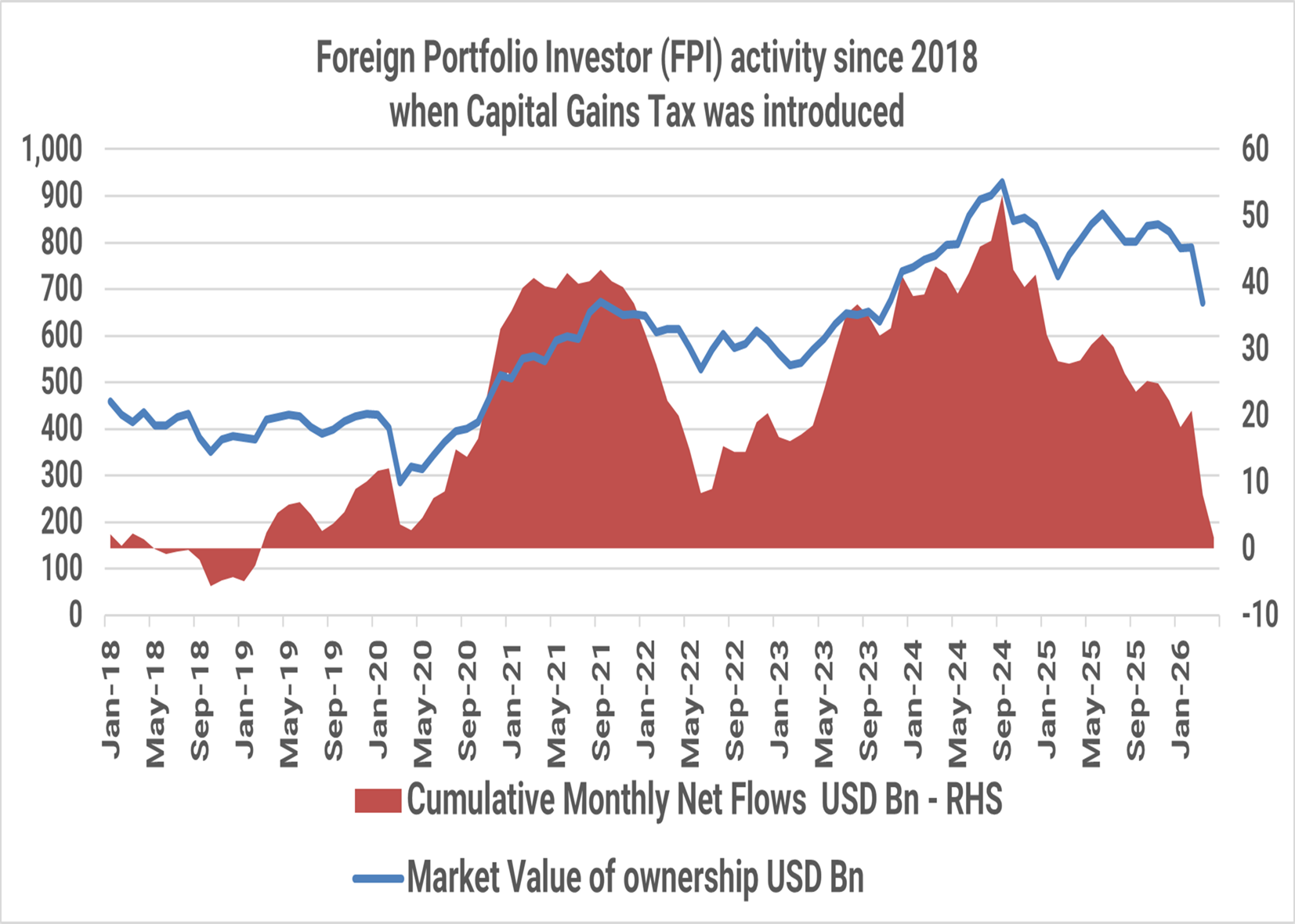

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.