China Tactical, India Strategic

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

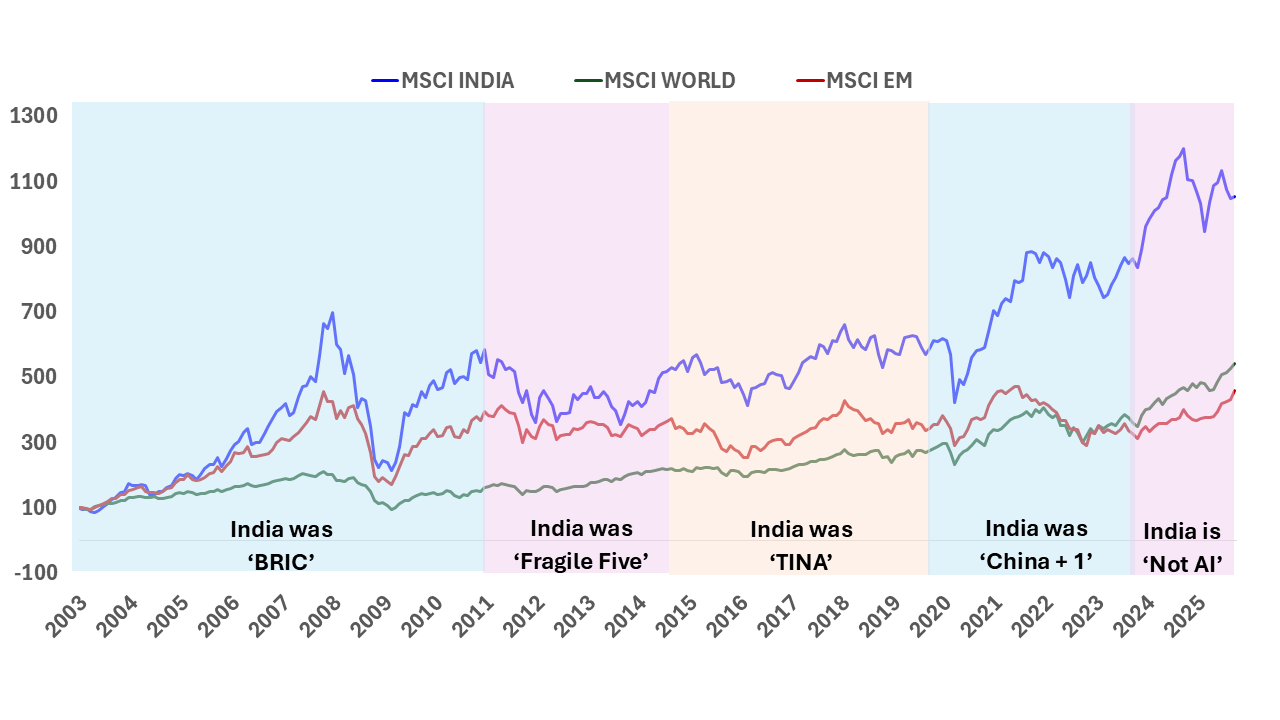

Aug 2, 2021Mesmerized by the Chinese dragon many investors have been comfortable leaving India in a generalist “emerging market” bucket in their allocation. The allocation was usually GEM + China with a few venturing to invest in other single countries. Given the large and growing size of the Indian economy and the opportunities it provides for investment, one would have expected investors to seriously look at a dedicated India allocation. Moreover, India has a historical track record of growth in GDP translating in returns in stock markets (Chart 1). However, the crackdown on businesses in China, particularly in the technology sector erased significant chunk from their market value and have again led investors to shy away from single country mandates. Consultants advising Global investors after facing the music from clients for the China exposure are also reluctant to recommend another single country like India. This is a lazy view and is doing injustice to their clients.

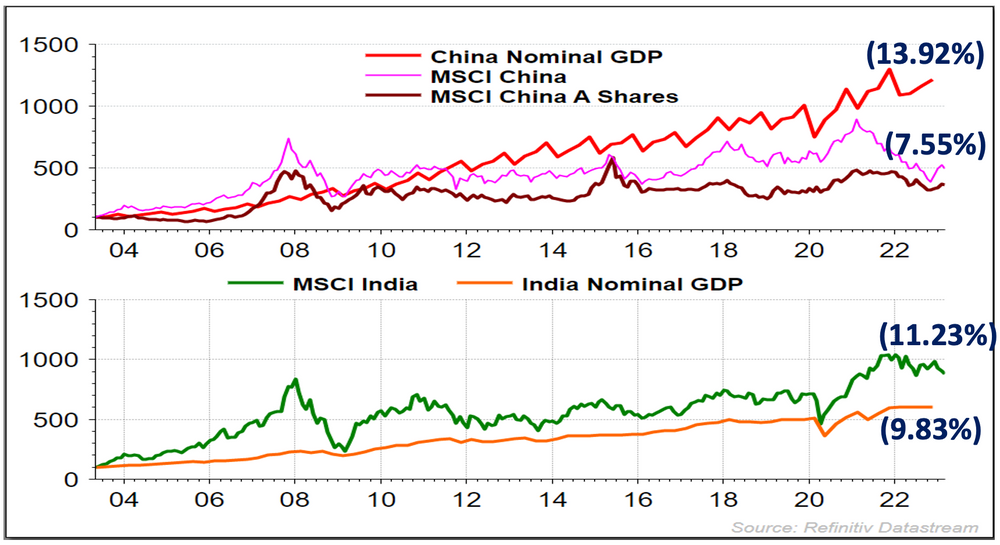

Chart 1: India GDP Growth Reflected In Equity Markets

Source: Refinitiv DataStream, All data in USD, GDP data is quarterly till Sep 2022, Index data is monthly till April 2023

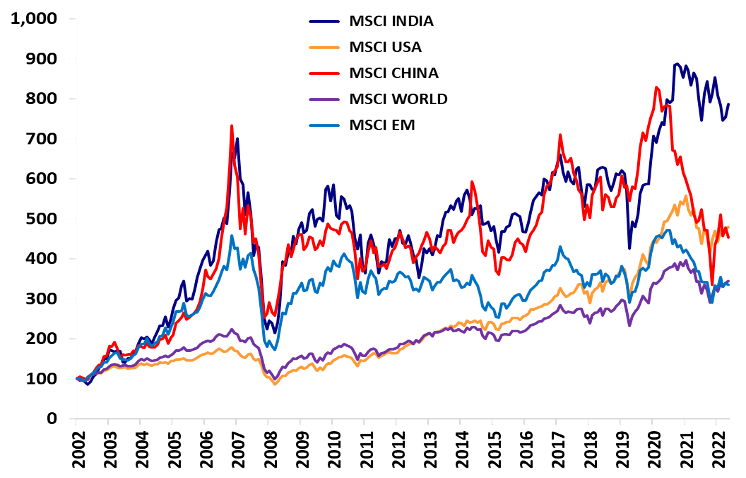

Chart 2: Under Allocation To India Has Hurt Investors

Source: MSCI Indices, 20-year data; rebased to 100 from December 2002 till April 2023

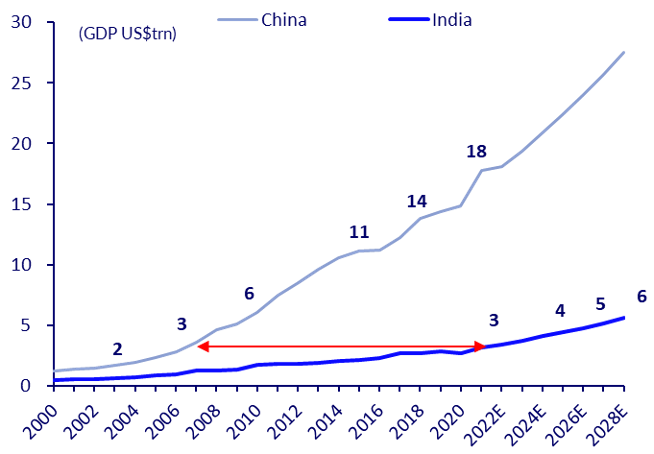

India, with a GDP of US $ 3.5 Tn is where China was in 2006 (Chart 3). With a young population of median age 28 vs 39 in China, India not only has the potential to grow at 6.0%-6.5% in real GDP terms over next two or three decades but is also poised to be a large consumption market.

Chart 3: India Today where China was in 2006

Source: IMF

China caught the tailwind of global exports driving GDP growth which may no longer be an opportunity. India may not match Chinese growth rates. However, India has focussed on developing its domestic consumption market and with many people entering the labour force domestic consumers will be the primary driver of GDP growth which is expected to be far superior over the next few decades versus any large global economy.

The population is not only young, but also digitally savvy making it feasible for India to solve many of the bottlenecks it conventionally faced; Delivery of public goods and services, health care to name a few. It is to cater to this population plus the need to de risk dependence on China that is making large companies such as Apple, Samsung and other MNC’s to tap into Indian market.

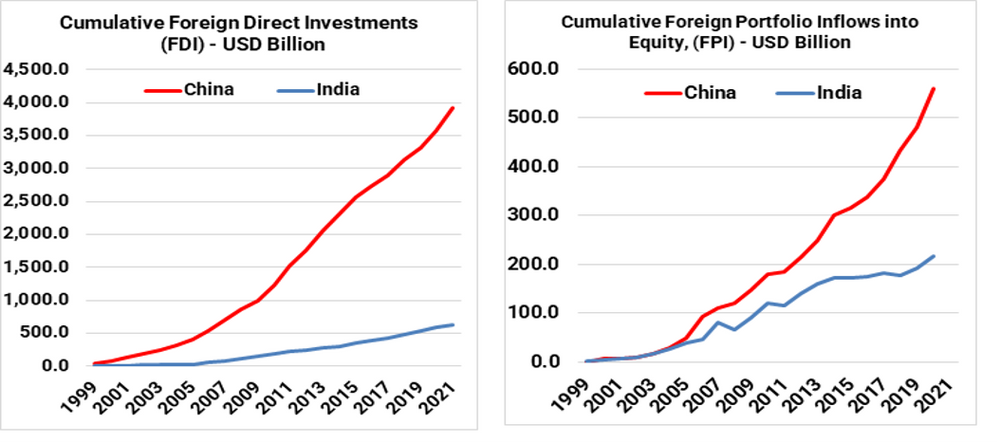

Chart 4: Foreign companies and investors will pour out their love for India

Source: World Bank, Data available till 2021

In addition to attractive demography, and a large market, India offers a superior regulatory framework along with a robust democratic system. Unlike China where the policies are almost decided by an individual and therefore susceptible to his whims and fancies. India remains a messy, unruly democracy with city, state and national objectives not always in sync – much like the US. The Government remains one of the largest litigant but like in most democracies the courts at all levels regularly rule against the government. Administration in India is decentralised: Finances and power are devolved from the Centre to the States and from States to Local governments. The legislators at all levels are democratically elected.

While the Modi Government does show some “Strong Man” tendencies, it is unlikely that India follows the path of China, Russia and Turkey. There are issues of corruption and challenges in education, healthcare, job creation, skilling to name a few – but there are also honest efficient officers, politicians and institutions at various levels that work towards delivering the growth.

India has its fair share of uncertainty for foreign investors who are not familiar with the cronies and their control over policy making. But generally, these are well known names, and a prudent manager should be able to identify and avoid investing with these cronies.

Indian stock exchanges too over time have consistently gained significant depth and settlement systems are world class, making large allocations easy to absorb (Table 1).

Table 1: Evolution of Indian Equity Investing Landscape

Chart 5: Liquidity, Governance and Valuation should be the base on which to build your India allocation

Source: Quantum Advisors

We thus reemphasise that, just like the multinationals, portfolio investors must have a more balanced “GEM + India” approach to building their long-term investment portfolios. We believe that the next 20 years offers an attractive opportunity for long term strategic allocators to create significant wealth from an India-dedicated mandate in an economy where growth is structural and broad based.

Related Post

India: T I N A to A N T I

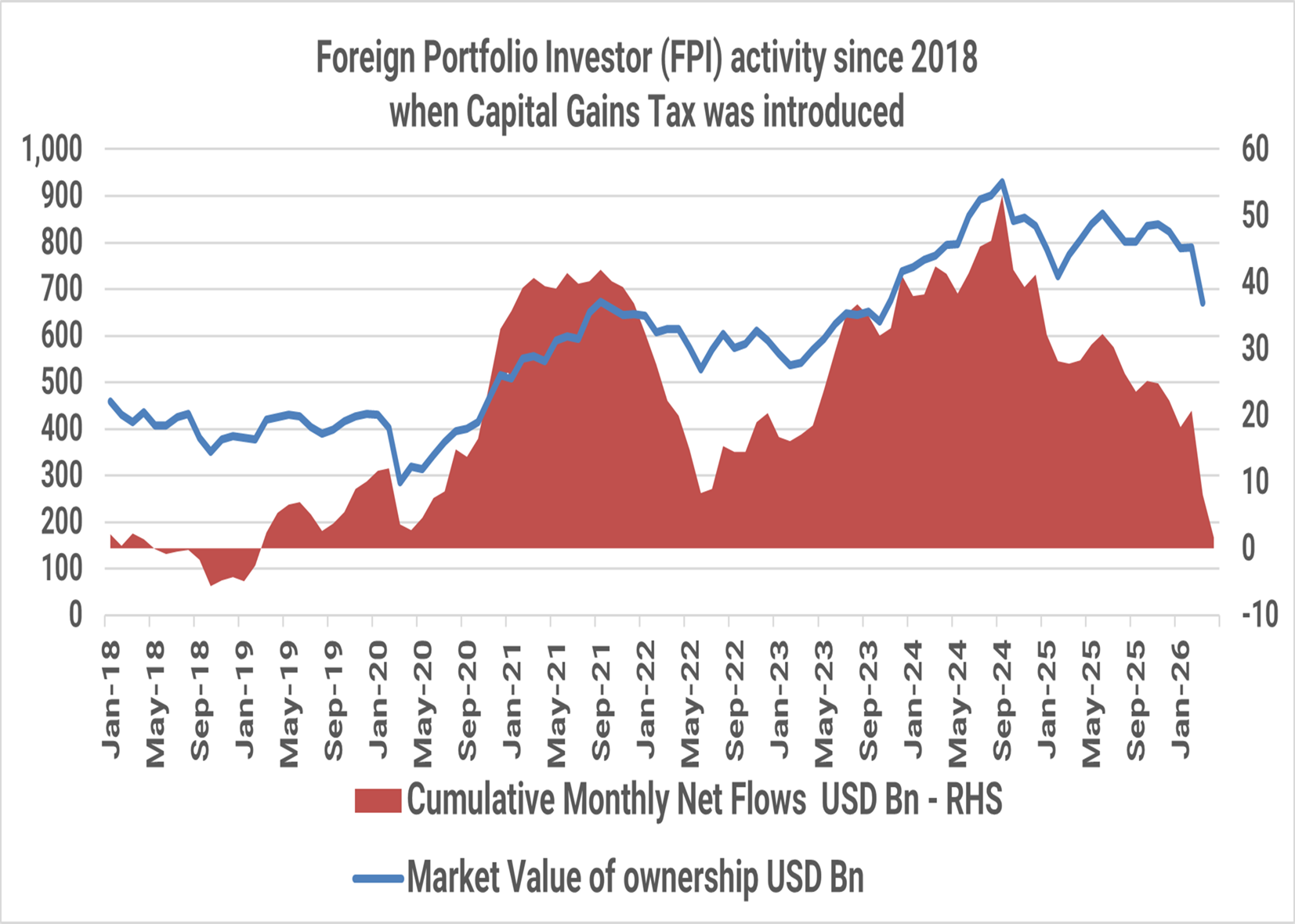

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.