China Contagion, US Exit of Afghanistan, or Fed Exiting QE?

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

Sep 29, 2021Assessing companies for financial risk, sustainability and resilience to macro turbulence is key to our proprietary ESG investment process.

Whether it be a taper tantrum, an inflation scare or a Covid blow, any portfolio - particularly in the emerging markets - needs to be prepared for the resulting fallout. However, portfolios that have companies with strong balance sheets, backed by able managements, usually emerge stronger from any crisis. The Covid crisis was one such stress test where quality businesses with robust financials emerged even stronger gaining market share and achieving higher profitability.

Financial sustainability remains an integral part of our ESG assessment in our India Responsible Returns offering. The objective of our financial filters in our proprietary ESG assessment is simple: It does not matter if a company has the best 'green' credentials in India but if has used excessive leverage and taken undue risks to grow the business, our proprietary ESG screen will not allow the bad apple to slip into our database of investable stocks: we will exclude the company from the portfolio. The forward looking financial scrutiny of companies helps mitigate portfolio risk of permanent loss of capital. Limiting your exposure or a complete exclusion of companies with weak financials outlook pays off in turbulent times.

Not that markets seem perturbed by the turbulence. Markets seem sanguine on the recovery, literally shrugging aside many of the lurking risks that could potentially impact the economy and markets. China is rumbling on one side and geopolitical risks have increased on the other - these could have lasting impacts on markets. Similarly, an exit from 'easy-money' can also have an impact on riskier segments of the markets, given that assets are priced to perfection today. Financial sustainability remains an integral part of our ESG assessment. As custodians of investors' capital, we recognize many of these risks and ensure that our portfolios are stress-tested to come out of these event-risks relatively unscathed.

For now, the financial universe is bracing for a soft landing of the potential monetary normalization i.e. the exit from easy monetary policies. The important question remains whether the Federal Reserve will be able to pull back without triggering the kind of “taper tantrum” that roiled markets worldwide in 2013. A lot is at stake, given the mountain of cash awash in the financial system.

But it is important to note that India in 2021, unlike in 2013, is a lot healthier. The EM poster boys, well known as Fragile Five back then, now have current account deficits significantly lower than it was in 2013. The CAD for these five economies averaged around 4.4% of GDP, compared to just 0.4% now. Nor are real exchange rates as overvalued as they were then, which had led to sharp depreciation in currencies amidst weaker fundamentals and accelerated outflows causing a double whammy. In India, the central bank has already bulked up a war chest by accumulating foreign exchange reserves to the tune of $642 billion. The forex reserve kitty stands at ~15 months of import cover as opposed to ~7 months in 2013. India’s forex reserve is enough to continuing paying the import bill and be able to pay its external debt maturity even considering any external shock.

The Evolution of Financial Filters

On Jan 8th 2014, The Guardian in UK published an article and the headline read “Let's be honest: Real sustainability may not make business sense” (1). The author goes on to argue that “…the interest of profit blatantly conflicts with the interest of people and planet”. And very early into our Q Responsible Return Strategy track record, one of the potential investors asked us “Will you invest in a company with say, 3 consecutive years of losses, but has great ESG score or performance?”.

CEOs and the Board of companies, in general in the past, didn't have the scrutiny that they are faced with today when it comes to running their businesses 'sustainably' - not just investors but also customers demanding environmentally conscious products and more inclusive workforce practices. At the same time, the managements must invest in technologies, human talents and generate profits to remain relevant in the long term in an increasingly VUCA world (Volatility, Uncertainty, Complexity, and Ambiguity).

People, Planet, Profit: The Triple Bottom Line

As an investment firm, our mandate is to invest the capital of our clients for sensible long term returns without taking undue risks. It has been over 25 years since Quantum Advisors and its founders have included a "Governance" factor when investing in companies. This is the "G" in "ESG". We have been believers of People, Planet, Profit and not one over the other (watch Ajit Dayal's, Founder of Quantum Advisors, views on triple bottom line).

In our view, any sustainable or responsible investing framework will need to have financial sustainability strongly imbibed in its evaluation process.

Financial Sustainability is Core to Our Proprietary ESG Process

The objective of our financial filters in our proprietary ESG assessment is simple: It does not matter if a company has the best 'green' credentials in India but if it does not generate wealth for shareholders that justifies the cost of capital and/or takes excessive risks to grow businesses i.e., leverage, we will exclude the company from the portfolio.

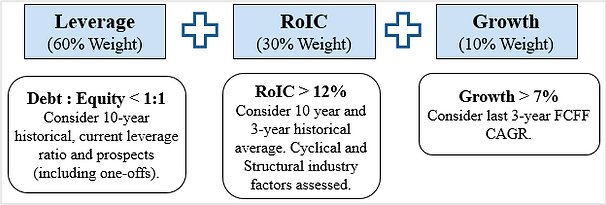

We apply the three quantitative financial filters on our ESG research database of over 150 companies and to its peers i.e. leverage, RoIC and Growth. The objective is to avoid companies within a sector with structurally high leverage and/or poor track record of shareholder wealth creation and/or inferior growth profile.

Financial Assessment is Also Forward Looking

It is quite possible that a company has embarked on a large capital expenditure program that may increase leverage in the short term beyond our comfort of 1 time but leverage is expected to reduce as the new capacity starts contributing to revenues and profit ability. Therefore, companies meeting close to the minimum threshold are assessed on the current and future financial prospects. This exercise helps us to avoid traps where financial soundness meets looks fine today but is about to deteriorate and at the same time capitalize on opportunities where things are expected to improve significantly over the foreseeable future.

| Leverage checklist | RoIC checklist | Growth checklist |

|---|---|---|

| Is the high leverage expected to prevail for the foreseeable future? | Is the low RoIC expected to prevail for the foreseeable future? | Is management taking steps to rectify low growth? |

| Is management taking steps to rectify high leverage? | Is management taking steps to rectify low RoIC? | Is the low growth due to cyclical downturn or irrational competition? |

| Is leverage high due to one-off major capital expenditure? Or an outcome of regulatory requirement? | Is RoIC low due to cyclical downturn or irrational competition? Is the industry / company dynamics improving? | Has the company maintained its market share during low growth period? |

We meet every companies in our ESG database once in six months. We engage with the company to understand the business plan while asking relevant questions on ESG metrics. We also engage and review consensus forecasts, meet competitors and dealers/suppliers. This 'not-a-desk-ESG-research' process helps us make forward looking qualitative assessment of a company's financial prospects. The ESG analyst also draws from the knowledge and experience of over two decades of the equity analyst tracking the company or sector to reach at a more realistic assessment of the company's financial prospects. This, in turn, mitigates portfolio risk of permanent loss of capital by limiting exposure or complete exclusion of companies with weak financials outlook.

Ultimately, the weight of the stock in the portfolio is subject to this financial assessment. We avoid companies with potentially permanent loss of capital while financial stable companies are allocated ESG-score based weight.

| Financial Assessment | Portfolio action |

|---|---|

| High risk of permanent loss of capital | Exclusion from portfolio |

| Low financial risk with improving financial outlook | Max 1% weight in portfolio |

| Significant improvement in financials prospects | ESG score determines the final weight |

As a result of our financial filters, the portfolio is less leveraged compared to the benchmark indices, have better/equal growth prospects and have had a long record of financial stability.

John Elkington in his book suggest the case for “Sustainable Capitalism”, wherein competing entities seek to maintain their relative position by addressing people and planet issues as well as profit maximization”. It is our endeavour to manage not just ESG risks but also ensure Q IRR strategy builds a portfolio that ultimately generates returns for our investors.

Related Post

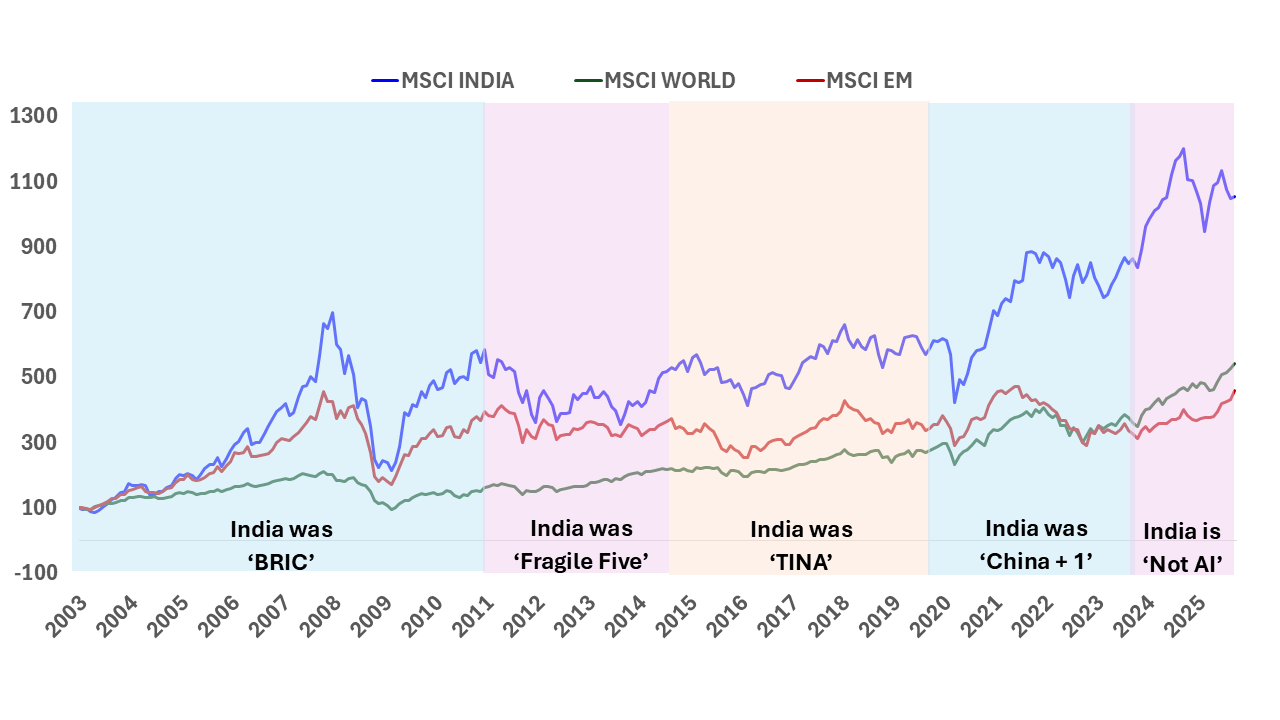

India: T I N A to A N T I

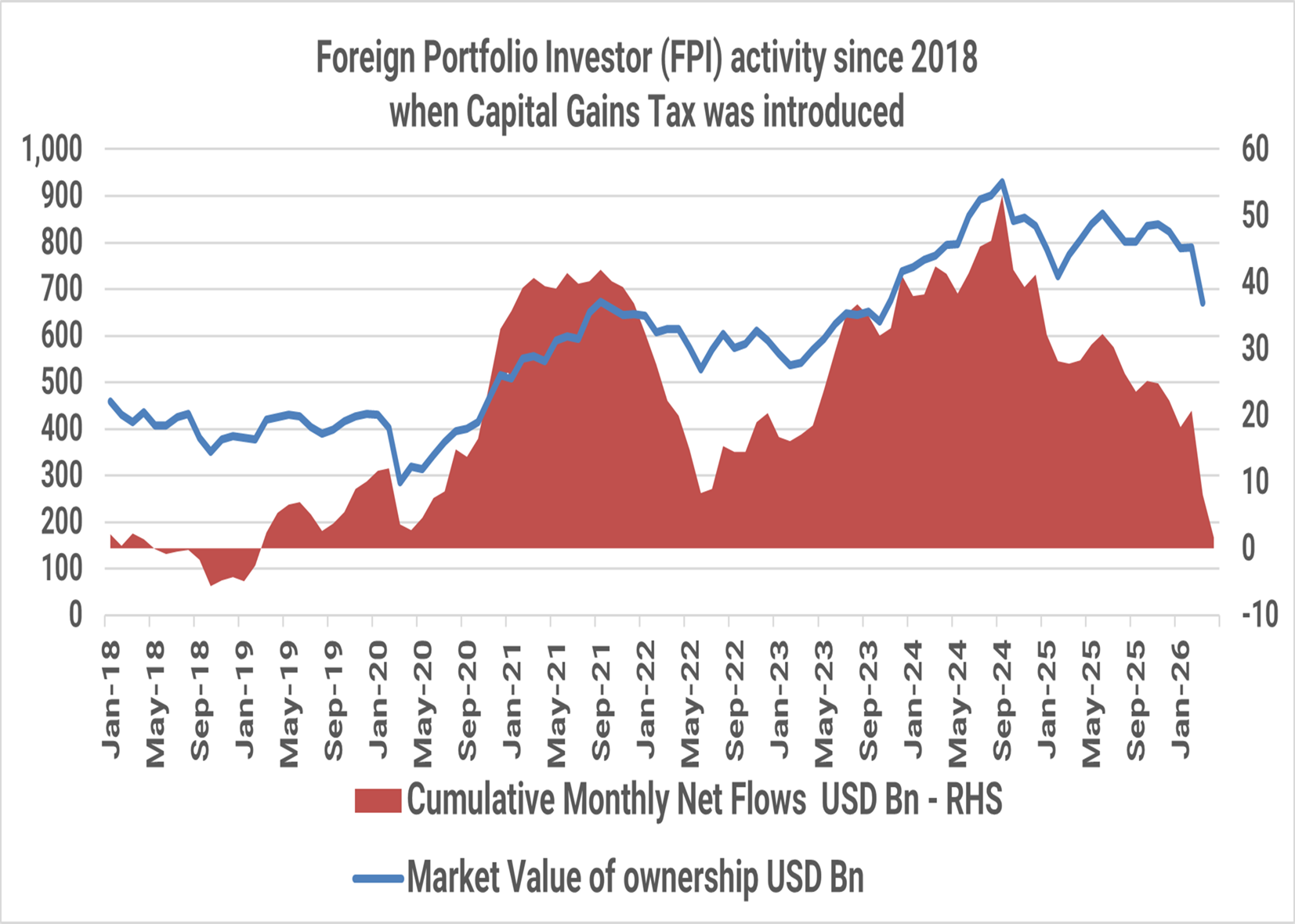

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.