India allocation: Ignore governance at your own reputational risk

“It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently” – Warren Buffet

Global institutional investors ignore risk when they invest in India. The recent bribery allegation against the Indian conglomerate and its founder along with employees of institutional investors, illustrates the governance challenges of investing in illiquid private assets in India. Macro risks and market risks can be priced and managed over the long term. However, governance risks can seldom be priced and the reputational costs of backing ‘bad actors’1 can be severe.

Despite the incident, we believe the opportunity set in India is wide and diverse. Global Investors can make sensible, risk adjusted returns by attempting to control risks which can impact their reputation by considering these issues:

Volatility is not the only risk

Most investment professionals equate risk with volatility. But risk is a fundamental issue that questions the very basis of the existence of an enterprise. And risk can show up over decades. Impatient asset allocators seeking ‘alpha’ and quickish returns can hop over to their next job if they ‘get it wrong’ and Boards of Trustees and members of oversight committees may retire long before risk ‘impairs the portfolio’.

Eventually the ultimate beneficiaries – the pensioners or family members – are left nursing the losses from the fundamental error of equating volatility with risk.

One of the biggest risks institutional investors faces is that of ‘governance’ – or lack of it. What type of companies are they investing in the public markets? What is the quality of the founders they are implicitly trusting when they invest in private assets? How have the companies they invest in secured permission for their infrastructure projects – a mostly opaque process riddled with bids and government-approved agreements? Which developer partner are they working with when they invest in real estate projects be it for warehousing, data centres, or commercial/residential real estate projects?

Reputation risk of backing Crony Capitalists with passive investing

Global Institutional Investors invest across markets passively by replicating an Index or buying an ETF. The key benchmark indices do not have a governance screen to weed out ‘bad actors’ 1. Index providers tend to react to a governance event post facto by removing the company from the Index when the damage is already done. Passive investors are failing in their fiduciary duty and exposing themselves to reputational risks. India investing should be active, with a clear focus on governance. A ‘Be Good. Do Good’ approach to investing in India can help deliver sensible returns.

Global Institutional Investments in Indian Private and Real Assets

India needs trillions of dollars to meet its sustainable growth aspirations. India’s Foreign Direct Investments (FDI) have risen, however, unlike in China where global corporations drove large investments into China to manufacture and operate, in India, a bulk of the FDI is investments by global investors into private equity, venture capital, infrastructure and real estate which gets classified as FDI.

Foreign investors have allocated twice as much to private markets and real assets over public equities2. India has received increased flows from foreign investors in infrastructure and real estate investments on the back of an improving regulatory eco system, emergence of investment trusts for operating assets and a growing pool of diverse asset operators3. However, we are unsure that investors have been duly compensated for the illiquidity and governance risks in private assets. Many instances of the quality of the founders being implicitly trusted, the nature of the infrastructure contracts being secured and the choice of the real estate developer partner suggest to us a dilution of risks that has impacted eventual returns.

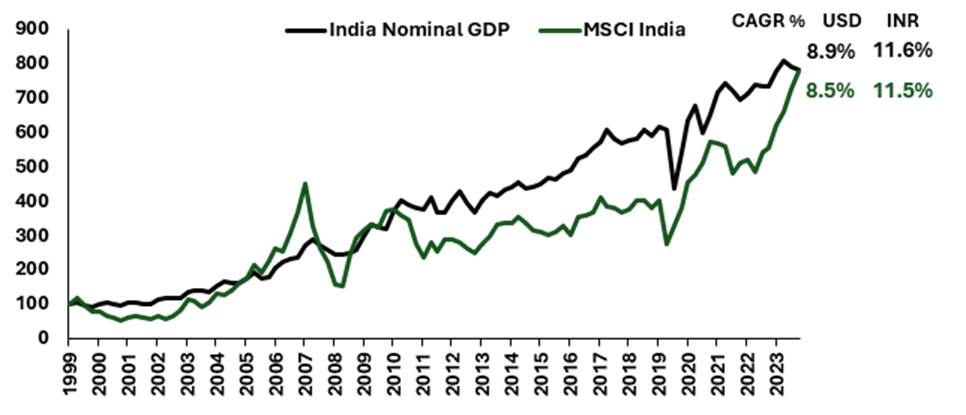

On the other hand, this real GDP growth since 2000 has led to double-digit growth in nominal GDP (CAGR 11.6% in INR) / (8.9%in USD ), which is reflected in the Indian Stock Market Returns as represented by MSCI India Index ( CAGR 11.5% in INR) / 8.5% in USD ).(data as at September 2024, see the charts at the end of the article). Despite India’s requirement of private capital, unless allocators to private investments assess and price the governance risk correctly, investing in public equities may offer a superior risk/reward outcome.

Indian capital market regulation and rule of law

There will be questions raised against India’s economic investigative agencies, the regulator and the stock exchanges on what the US Department of Justice (DOJ) and US Securities Exchange Commission (SEC) discovered about an Indian company which the Indian agencies missed. Investors need to be reassured that the Indian agencies are independent and able to gather all the information they need to arrive at a decision about rule of law being maintained. The regulatory ecosystem should have enough deterrence, checks and balances to protect investors from governance risks. Alas, the onus to manage the reputational risk of governance issues is in the hands of the investor and/or their local partners and not on any reliance on mathematical formula of standard deviation and volatility.

An indictment of a corporation, but not an indictment of Indian capital markets

Poor governance, fraudulent accounting, and unchecked greed are not restricted to emerging markets like India. Enron, Exxon, AIG, Lehman, Madoff, Wirecard, Parmalat, Theranos were some of the many shocks to the western capital markets.

This incident may be indictment of a corporation, but this should not be seen as an indictment of the Indian capital markets. Over the years, SEBI and the market intermediaries have created a robust capital market infrastructure which has increased investor confidence, seen a surge in listings and market volumes and has witnessed a diverse participation from the biggest global institutional investors to the smallest domestic retail Indian individual.

We believe Indian public equity markets are relatively ahead of the curve as compared to many other global exchanges in terms of compliance, disclosures, operations and settlement.

The knee-jerk reaction of such an alleged failure of governance can be to redeem out of all India investments thereby missing the opportunities for significant compounding long term returns from investing in India – an act of throwing the baby out with the bath water.

The more studied and measured response to such an event is to adopt and/or to find external managers who have an established process of governance-screening embedded in their research and investment selection criteria.

Global Investors can make sensible, risk adjusted returns by attempting to control risks which can impact their reputation.

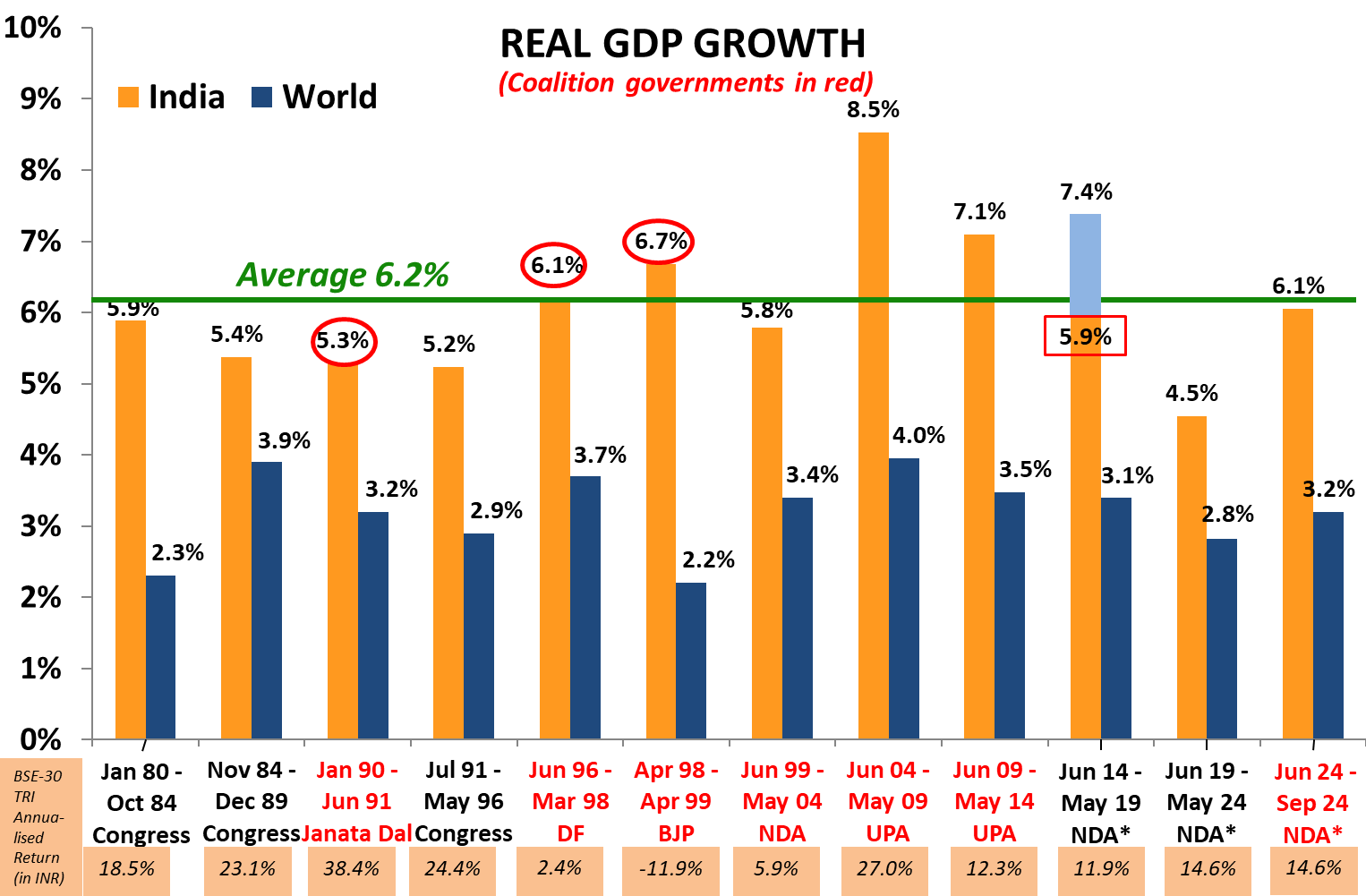

Chart 1: India Real GDP growth has averaged between 6.0%-6.5% across different governments. Since 2000, the real GDP growth has averaged 6.2%; similar to its average since 1980

(Source: Worldbank, RBI and www.parliamentofindia.nic.in as of September 2024. Note: The number in red rectangle is from a changed data series starting Jan 2015. While a “superior” series, there is no comparable number to equate the “New” with the “Old”. Most economists deduct 0% to 1.5% from the “New” to equate to the “Old”; therefore, under Modi, the GDP has been at 5.9% at best matching the 5.6% under the BJP-led coalition government of Vajpayee that resulted in a rout for the BJP at the time of the next election in 2004. Please note that data used for World GDP from 2021 is a median annual estimate since quarterly data is not available and India GDP data is governments second advance estimate released at the end of November 2024)

Chart 2: This real GDP growth leads to an increase in nominal GDP which is reflected in market returns

(Source: Bloomberg, Chart data in USD, Quarterly Data till 30-September 2024, Y-Axis Rebased to 100 on 31-Dec-1999)

This is only for representation and understanding purpose and does not assure any promise or guarantee of same in the future.

Past performance does not guarantee and is not indicative of future results

Notes to the Article

- Bad actors is referred to companies considered to be poor on Governance/ESG parameters as per Quantum’s internal research and investment process. Read more about our Integrity Screen here India Governance.

- NSDL for FPI flows, IVCA report for Private Asset flows to India, RBI data on FDI flows

- IBEF, FDI update, November 2024

Important Disclosures & Disclaimers

The views expressed herein shall constitute only the opinions and any information contained in this material shall not be deemed to constitute an advice or an offer to sell/purchase or as an invitation or solicitation to invest in any security and further Quantum Advisors Private Limited (QAPL) and its employees/directors shall not be liable for any direct or indirect loss, damage, liability whatsoever arising from the use of this information.

Information sourced from third parties cannot be guaranteed or was not independently verified. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. All the forward-looking statements made in this communication are inherently uncertain and we cannot assure the reader that the results or developments anticipated will be realized or even if realized, will have the expected consequences to or effects on, us or our business prospects, financial condition or results of operations.

Recipients should exercise due care and caution and if necessary, obtain the professional advice prior to taking any decision based on this information

Important Notice:

This newsletter contains hyperlinks to websites operated by third parties. These linked websites are not under the control of QAPL and are provided for your convenience only. Clicking on those links or enabling those connections may allow third parties to collect or share data about you. When you click on these links, we encourage you to read the privacy notice of the website you visit. QAPL does not endorse or guarantee products, services or advice offered by these websites.

UK related important disclosures:

• The content of this newsletter has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 (“FSMA 2000”). Reliance on this newsletter for the purpose of engaging in any investment activity may expose you to a significant risk of losing all of the property or other assets you invest or of incurring additional liability. This newsletter is exempt from section 21 FSMA 2000 on the grounds that it is directed only to certified sophisticated investors, high net worth companies, unincorporated associations, trusts and/or investment professionals within the meaning of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (“FPO”). The investment activity described in this newsletter is only available to these persons or entities and no other person or entity should rely on the contents of this document.

• The protections conferred by or under the Financial Services and Markets Act (FSMA) will not apply to this newsletter and any investment activity that may be engaged in as a result of this newsletter. The applicability of any dispute resolution scheme or compensation scheme and its jurisdiction (if and where applicable) pertaining to a transaction resulting from this newsletter would be as specified in the respective client agreements.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.