India needs sustained long-term growth to pull people out of poverty, create jobs for the young, and boost incomes to widen the consumption base. At Quantum, we have long held India’s potential real GDP growth rate to be 6.0%-6.5% (6.2% is the average since 1980). This pace of growth, though twice that of world GDP, may not be enough to achieve India’s aspirations of becoming a middle-income country and creating meaningful jobs for its youth.

The Indian state, the Indian economy and most Indian corporations do not fall under any of these categories and hence are unlikely to be directly impacted by Trump’s policies.

India is a big net importer of Oil and Gas and can technically benefit from a supply hegemon like US. India does not have any stake in the high technology world. India does not make high end chips, has not developed its own large language models, does not even have its own 5G telecommunications protocol, and has no major technological prowess in new energy – renewable, battery, storage. India runs an overall trade deficit. India runs a small trade surplus with the US in goods and a larger trade surplus in services and we will discuss that in detail below. India is not part of any multi-lateral trade agreement and has not ‘gamed’ US free trade. We believe India is not a ‘geo-political threat’ to the US. Also, India has never been dependent on US congress’s benefactions to manage its own security interests.

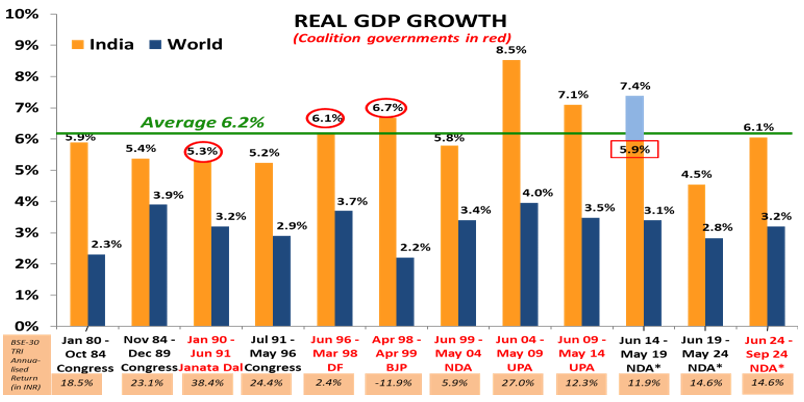

Chart 1: India GDP growth has averaged 6.2% since 1980

Source: World bank, RBI and www.parliamentofindia.nic.in as of September 2024. Note: The number in red rectangle is from a changed data series starting Jan 2015. While a “superior” series, there is no comparable number to equate the “New” with the “Old.” Most economists deduct 0% to 1.5% from the “New” to equate to the “Old”; therefore, under Modi, the GDP has been at 5.9% at best matching the 5.6% under the BJP-led coalition government of Vajpayee that resulted in a rout for the BJP at the time of the next election in 2004. Please note that data used for World GDP from 2021 is a median annual estimate since quarterly data is not available, and India GDP data is governments second advance estimate released at the end of November 2024. The graph is only for representation and understanding purpose and does not assure any promise or guarantee that the historical performance is indicative of future results.

Can India then grow at +7% for a sustained period? The answer to this proverbial question on India’s potential growth rate depends on the period in which the question was asked:

- In the 1980s, the hopeful answer would have been 5%.

- In the 90s, post-liberalization, hopes had risen for a sustainable 6% growth rate.

- During the ‘Goldman Sachs - BRIC’ mania of 2004-2011, it was India’s birthright to grow at 9%.1

- Morgan Stanley’s ‘Fragile Five’ in 2013 smothered it down below 8%.2

- ‘Ache Din’ in 2014 raised hopes of 8% again

- In ‘Atma-Nirbharta’ and ‘Amrit Kaal,’ many seem to be settling for ~6%.

Our long-term assumption of 6.0%-6.5% real GDP growth comes from a very simple analysis. Assuming India’s Gross Domestic Savings (GDS) of ~30% of GDP and the incremental Capital-Output ratio (ICOR - capital required to get a unit of growth) of ~5, the potential growth (GDS/ICOR) gives us 6%. This ~6% gets balanced by the negative aspects of inefficiency in the government sector and household savings, and the positives of attracting excess foreign savings into India.

Technically, India should be growing faster than this suggested potential. Efficiency is improving (India’s ICOR is lower) 3; Indians are saving more in risk assets4, and India is attracting capital from abroad across Foreign Direct Investments (FDI), Foreign Portfolio Investments (FPI), Foreign Borrowings (ECB), and from the Indian diaspora (remittances and deposits) (see chart 4). However, these have not resulted in growth sustaining above 7%.

Table 1: India GDP growth has been below potential in the last 10+ years

| % yoy | During ‘Fragile Five’ | Post ‘Fragile Five’ | Demonetisation, GST, RERA, Credit Crisis | COVID Period | Post COVID | Under NDA Government |

|---|---|---|---|---|---|---|

| Average for the period | (QE Jun 2012 – Jun 2014) | (QE Sep 2014 – Sep 2016) | (QE Dec 2016 – Dec 2019) | (QE Mar 2020 – Sep 2022) | (QE Sep 2022 – Sep 2024) | (QE Sep 2014 – Sep 2024) |

| Real GVA | 5.99 | 7.85 | 5.75 | 3.96 | 6.53 | 5.88 |

| Real GDP | 6.19 | 7.99 | 6.19 | 3.61 | 6.88 | 6.03 |

| Nominal GDP | 13.43 | 10.77 | 9.87 | 11.06 | 9.32 | 10.28 |

(Source: CMIE Economic Outlook, QE=Quarter Ended; shaded for levels below 6.5%; GVA = Gross Value Added; ‘Fragile Five – refers to period when India was bracketed with countries which were vulnerable due to high external current account deficit and inflation in an era of tightening FED policy and strong dollar; RERA – Real Estate Regulation Act; Credit crisis refers to the financial system impact post the collapse of Il&FS, September 2018; Post COVID - we assume the quarter post September 2022 to be period from which y-o-y numbers are not impacted by covid period base effects; Under NDA government which started in May 2014, GDP data taken from June-September 2014 quarter)

For the quarter ending in September 2024, the year-on-year growth rates were as follows: Real GVA at 5.6%, Real GDP at 5.36%, and Nominal GDP at 8.04%. This represents a decline of more than 1.5% in both real and nominal terms compared to September 20235. This decline has sparked a debate on whether India is experiencing a cyclical or structural slowdown.

Some attribute the slowdown to tight fiscal and monetary policies, while others point to the incomplete recovery from the lack of income and job growth both pre- and post-COVID. A prominent economist and former Executive Director at the IMF described the slowdown as ‘surprising and inexplicable,’ attributing it to ‘India’s Deep-state inspired policy’ of high taxation on income, trade, and capital6.

All the above explain the current slowdown and it seems to be a mix of cyclical and structural reasons. However, the debate on whether the slowdown is cyclical or structural yet hinges on one’s growth expectations. If one expects sustainable growth above 7%, then India appears to have been in a structural slowdown for many years. Conversely, if one believes India’s sustainable potential is between 6.0% and 6.5%, the current decline might be seen as cyclical.

However, considering India’s young demographic and low per-capita levels, achieving a growth rate of 6% should be relatively straightforward. Therefore, a decline below this level, as observed in 2019 and now, is indeed a cause for concern.

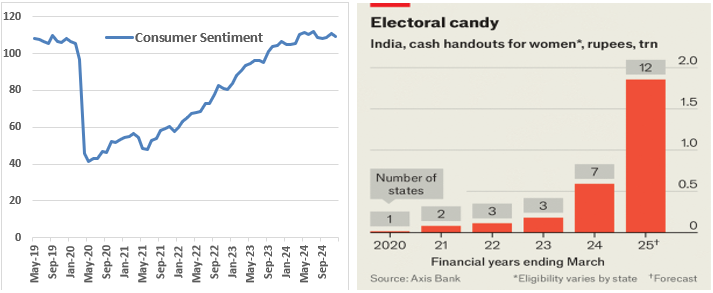

We do see some short-term remedies on course. Fiscal policies at the state level, across all parties in power, have turned towards supporting incomes and providing subsidies. 16 out of the 28 states now offer some form of direct income transfer to women. Various research now estimates that >0.5% of state GDP is spent only on women through bank transfers and other schemes7. This should alleviate some of the income concerns that seemed to have held back demand. This is the harsh reality, and politicians are the first to react to it. They know that over the last decade, growth has been weaker, incomes have been modest, and job growth hasn’t kept pace with the labor force. The only way to maintain social stability and political relevance is to provide cash transfers and income support, as the leader of the opposition, Rahul Gandhi, promised to voters as ‘khatakat’ – (like the brisk whirring sound of an ATM machine dispensing cash)8. Consumer sentiment and overall employment, which were already on the upswing and back above pre-COVID levels, should improve further, driving demand.

Chart 2 and 3: Consumer Sentiment should get a boost on cash handouts

(Source: Consumer sentiment - CMIE Economic Outlook; Data till December 2024; Chart from The Economist, article Jan 23rd, 2025)

Monetary policy may have sent the first signals of choosing domestic monetary policy over a fixed exchange rate. Allowing the INR to move freely and weaken against the US dollar is indicative of this stance. This needs to be followed up with liquidity infusion and a rate cut in February, which may further weaken the INR and ease economic conditions. We would expect these measures to address the ‘cyclical’ headwinds.

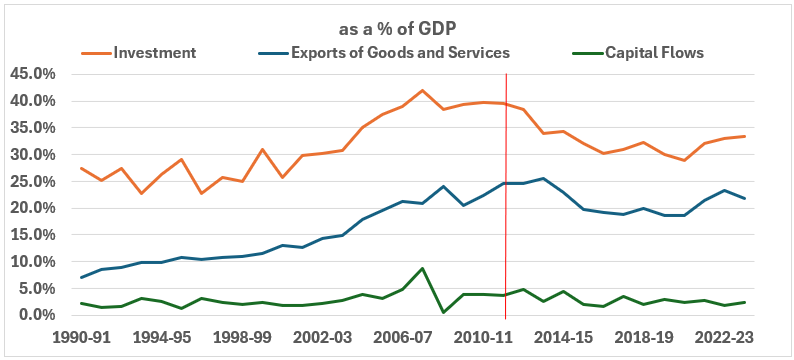

For India to grow at +7%, according to the ICOR formula, we need Gross Savings or investments to be at 35% of GDP, up from the current ~30% levels. This increase in investments and savings needs to come from higher domestic capital investment, an increase in the global share of exports, and a higher share of global savings as capital flows.

We saw this happen for close to two decades from 1991-2011, when investments rose due to an increase in domestic capacity creation, a rise in export share, and global capital flows. This does not need ‘big bang’ reforms now. India and India’s ‘Deep-state’ may know what it takes to try and drive growth above potential. It was a combination of receding government control, simplification of taxation, freer goods and services trade, and a recognition of treating risk capital in a fair, transparent, and consistent manner which lifted India’s potential growth from 5% to >6%.

Chart 4: Can going back to policies of pre-2011 get growth above potential or do we need a ‘New Deal’?

(Source: CMIE Economic Outlook; Annual GDP at current market prices; Investment=Gross Capital Formation; Total Capital Flows; Data till March-2024 )

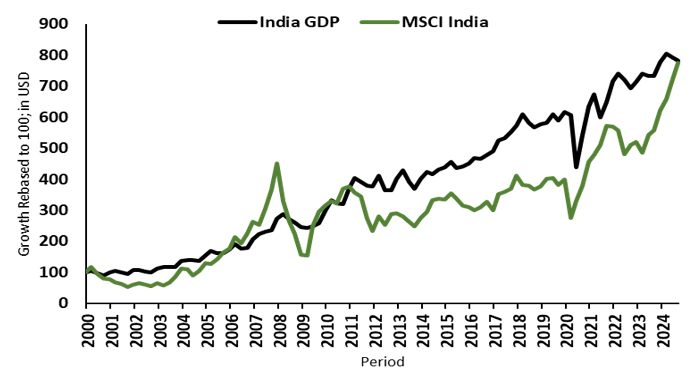

Having realistic long-term growth estimates is essential for investing in India. Historically, there has been a strong correlation between India’s nominal GDP growth and stock market returns. Since 2000, India’s real GDP growth has averaged around 6.2% per annum (INR). This consistent real GDP growth has driven double-digit nominal GDP growth, with a compound annual growth rate (CAGR) of 11.6% in INR and 8.7% in USD. This economic growth is mirrored in the Indian stock market returns, as shown by the MSCI India Index, which has a CAGR of 11.5% in INR and 8.6% in USD.

Chart 5: India: Where GDP growth has been rewarded by stock market returns

(Source: Bloomberg, All data in USD and up to September 2024)

However, there are times when investors develop unrealistic expectations based on short-term trends, themes, or fads. During the ‘BRIC mania,’ driven by the anticipation of sustained ~9% GDP growth, foreign investors poured money into Indian small caps, illiquid private equity, greenfield infrastructure, and Tier 2/3 real estate. Unfortunately, within a few years, many experienced significant losses in returns, capital, and reputation.

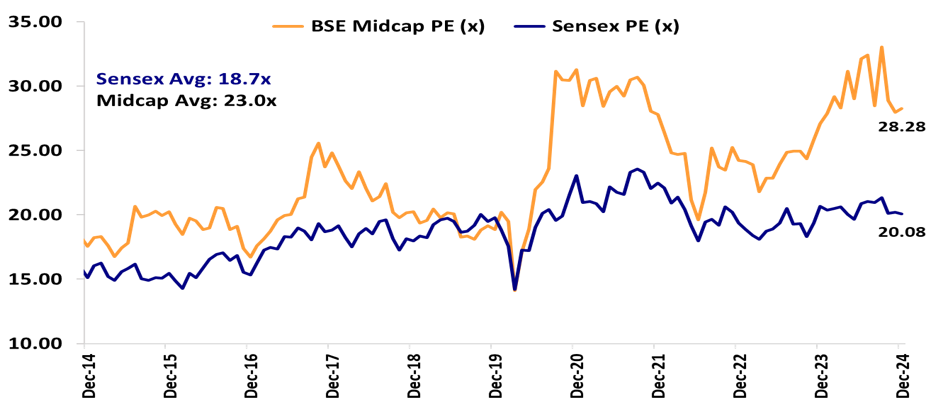

We might be witnessing a similar situation with Indian mid and small caps. Retail investors in India appear to be over-allocated to this segment, expecting faster growth and better stock price performance. As GDP growth slows and earnings growth declines, we are observing the effects on valuations and stock price performance.

We do not see a case for sustained GDP growth in India exceeding 7%. We believe it is prudent to price corporate revenues and profitability based on a normalised GDP growth rate of 6.0%-6.5%.

Chart 6: Midcap PE at ~23% premium to Large cap

Note: BSE Midcap Index and Sensex 1Y Forward PE.

Source: Bloomberg Finance L.P.; As of December 31, 2024

Past performance does not guarantee and is not indicative of future result

Sources and Footnotes

1 - Goldman Sachs Investment research ‘Dream onto 2050’, 2003 – BRIC

2 - BBC news article on Fragile Five, 2013

3 - SBI Report, March 2024 – (efficiency is rising; ICOR is falling)

4 - NDTV profit article, December 2024 – (Indian Household savings pattern)

5 - MOSPI press release, December 2024 – (Sept 2024 over Sept 2023 – GDP growth comparison)

6 - Article by Surjit Bhalla, January 2025 – (prominent economist and ex ED-IMF)

7 - Outlook Business article, December 2024, (State spend on women as a socio-political move)

8 - Indian Express Article, June 2024 – (Rahul Gandhi’s remark on Khatakhat)

Important Disclosures & Disclaimers

The views expressed herein shall constitute only the opinions and any information contained in this material shall not be deemed to constitute an advice or an offer to sell/purchase or as an invitation or solicitation to invest in any security and further Quantum Advisors Private Limited (QAPL) and its employees/directors shall not be liable for any direct or indirect loss, damage, liability whatsoever arising from the use of this information.

Information sourced from third parties cannot be guaranteed or was not independently verified. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and the views given are fair and reasonable as on date. All the forward-looking statements made in this communication are inherently uncertain and we cannot assure the reader that the results or developments anticipated will be realized or even if realized, will have the expected consequences to or effects on, us or our business prospects, financial condition or results of operations.

Recipients should exercise due care and caution and if necessary, obtain the professional advice prior to taking any decision based on this information.

Important Notice:

This newsletter contains hyperlinks to websites operated by third parties. These linked websites are not under the control of QAPL and are provided for your convenience only. Clicking on those links or enabling those connections may allow third parties to collect or share data about you. When you click on these links, we encourage you to read the privacy notice of the website you visit. QAPL does not endorse, or guarantee products, services or advice offered by these websites.

UK related important disclosures:

• The content of this newsletter has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 (“FSMA 2000”). Reliance on this newsletter for the purpose of engaging in any investment activity may expose you to a significant risk of losing all of the property or other assets you invest or of incurring additional liability. This newsletter is exempt from section 21 FSMA 2000 on the grounds that it is directed only to certified sophisticated investors, high net worth companies, unincorporated associations, trusts and/or investment professionals within the meaning of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (“FPO”). The investment activity described in this newsletter is only available to these persons or entities and no other person or entity should rely on the contents of this document.

• The protections conferred by or under the Financial Services and Markets Act (FSMA) will not apply to this newsletter and any investment activity that may be engaged in as a result of this newsletter.

The applicability of any dispute resolution scheme or compensation scheme and its jurisdiction (if and where applicable) pertaining to a transaction resulting from this newsletter would be as specified in the respective client agreements.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.