We have been on the road since 1990 when our founder Ajit Dayal published an article in the (Asian) Wall Street Journal signalling how economic reforms would ‘Loosen the Reins on India’s Bull Market – (see annexure). Over the past 35 years we have been preaching the gospel of investing in India’s growing economy via allocations to the Indian stock markets – and citing the dangers of bouts of hyperbolic euphoria that seem to periodically rule passionate hearts and override rationality.

A common refrain against an India allocation has been: “We don’t have room for Single Country Allocations – though we like the India opportunity”.

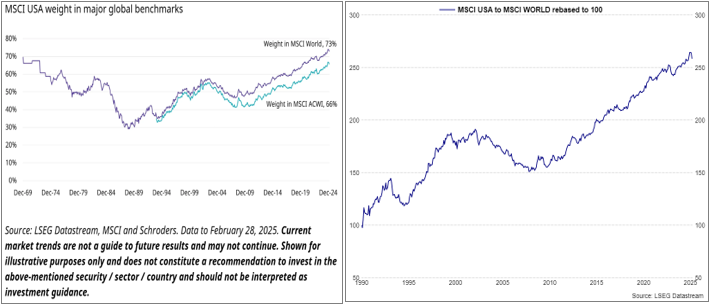

Yet, the allocations to ‘single country USA’ continued relentlessly. Being the largest economy in the world and, until recently, accounting for 70% of global market cap1, the US allocation by non-USA investors has been a profitable no-brainer .

This chart by Schroders, USA in an article2 on US exceptionalism shows the extent of US over-weight in global benchmark indices. Our chart on the right shows the justification given the out-performance of US stocks markets over other economies, especially over the last decade.

US Exceptionalism is reflected in Public Markets – Rise in US weight in Global Indices on superior performance

(The MSCI USA to world line is the performance of MSCI USA Index over MSCI world Index in US Dollars rebased to 100 in 1990). It depicts the relative outperformance of US listed stocks)

However, that was then. This is the now – and it is possibly an era of The New Abnormal. In private, irrespective of their location on the political spectrum, every investor is nervous. In public, many are questioning the extent of US exceptionalism.

With trade wars and battle lines drawn, non-US allocators of US assets face a risk not seen since President Roosevelt confiscated assets of the Japanese living in USA during World War 23 and President Nixon unlocked the doors of inflation by taking the US$ off the gold standard on August 15th, 1971 and set the foundation for unleashing untamed inflation internationally.4

More recently, the quiet country of Switzerland faced the wrath of the US (and the EU) for its ‘secret bank accounts’ and, by 2017, the Swiss had to buckle under pressure and change a 350 year practice and an 80 year law to suit the US5– or else…

After Russia invaded Ukraine in 2022 (and there is no getting away from that fact) in 2022, many European countries have confiscated Russian assets.

Single Country Allocations to the US – or to China and India – are fraught with risk. The problem is that ‘risk’ is, in a very narrow financial sense, only defined as standard deviation / volatility and fx movements.

Now there is the real ‘risk’ of permanent loss of capital by a Presidential directive – in any geography. Allocators, in our view, will reassess risk to include the long-forgotten political / social risks that exist in many regions of the world.

Will Canadians feel comfortable owning property in USA?

Will the Germans feel comfortable owning the S&P 500 Index?

Will a German company doing business with a Canadian company face the ire of a US government which sees that as bypassing tariffs?

Is it possible that an Administration, angry at the defiance emanating from certain allies, lashes out by placing a special tax on assets owned by a specific set of people? Or, worse, outright confiscation?

Will allocators who are not domiciled in the US relook at their sole Single Country Allocation to the US

Will they sell some of their US allocations?

If they sell out of the US, where will they allocate to?

Will allocators add more to Single Country Allocations and geographies like India?

Foreign Investors own US$ 31 trillion of US securities (~US$17 trillion of Public Equities; and ~US$14 trillion of US Debt)6.

Furthermore, we can assume that of the ~US$ 13 trillion of global private and alternatives capital; 60% (~US$8trillion) is invested in the US7.

So, foreign investors possibly own ~US$ 39 trillion worth of US assets.

This mostly excludes real estate holdings of foreign individuals which may only be reflected partially in the ~US$ 39 trillion.

If non-US based allocators decide to reduce their allocation to the US by just 10%, it would translate into a US$3.9 trillion flow back to home countries or allocated to other destinations and opportunities.

And India should attract some of that capital looking for reinvestment opportunities. Could India attract 5% of that US$ 3.9 trillion over a few years? If so, that amounts to a further inflow of US$200 billion from this one time- (and possibly some annual reduction in allocation?) - out of the US.

India has absorptive capacity to attract global capital.

India gets less than 2.5% of GDP annually in foreign capital inflows8. This is across Foreign Direct Investments (FDI), Portfolio flows and External Commercial Borrowings by the Corporate sector. At this stage of its development journey, India should be attracting at least 5% of GDP from foreign flows. This would amount to US$200 billion in annual foreign flows into India - 5% of current US$4 trillion GDP9.

Even if split equally into public and private markets, the India opportunity is large enough to absorb the flows. A US$100 billion annual flow as FDI into Private Equity (PE), Venture Capital (VC), Infrastructure and Real Estate (RE) in a growing US$4 trillion economy seems trivial.

A similar US$100 billion flow into Indian Public Equity Markets (~US$4 trillion market capitalisation10) and Indian Bond market (~USD 2.5 trillion outstanding11) suggests there is the ability and the capacity to be easily absorbed.

Not many countries can absorb such amounts of foreign capital from a size perspective. Also, India is amongst the few ‘friendly’ destination country for most other nations in the world. The tax angle remans a key frustration but – given the possible alternative of a risk of confiscation of capital v/s tax on capital gains – India remains a good option.

MSCI Indices are backward looking: We would argue that global allocators need to allocate 5% of their portfolio to India.

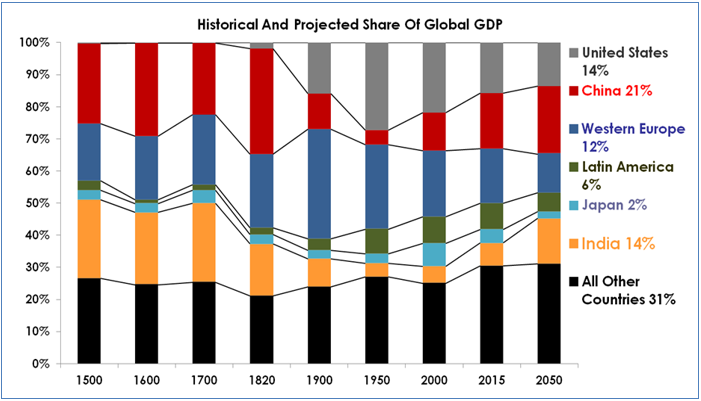

When ‘Loosen the Reins on India’s Bull Run’ was published in the (Asian) Wall Street Journal in February 1990, India’s weight in the MSCI All-Country World Index was barely 0.1%. Today it is nearly 2%. Investors who ignored India based on historical data of the indices lost a great opportunity. Today, with indices still forcing you to look in the rear view mirror, global allocators face the same choice.

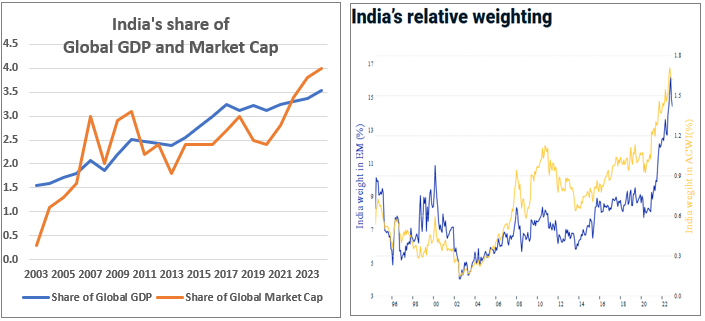

India’s weight in Global GDP and Global Market cap is ~4% (see chart below). India’s GDP and Market capitalization is growing faster than global. India will command over 5% share of global GDP and market capitalisation within the next 10 years.

Our argument is that global allocators need to make investment allocations which should be futuristic. Investors need to allocate a higher weight today to benefit from India’s growth and opportunity.

Indian Public Equities has a less than 1% allocation in Global Portfolios

| Data in USD Billion | Investments in Indian Public Markets | Global AUM | % of Global AUM in India | ||

|---|---|---|---|---|---|

| Investor Category / Investments | Equity | Debt | Total | Global AUM of these investors | India public Investment as a % of their global AUM |

| Central Banks/ Sovereign Wealth Funds/Governments | 141.6 | 15.8 | 159.9 | 13,000 | 1.09% |

| Global Pension Funds | 72.9 | 4.4 | 77.9 | 60,000 | 0.12% |

| Endowments/Foundations | 6.3 | 0.0 | 6.3 | 1,500 | 0.42% |

| Insurance Companies | 10.4 | 1.0 | 11.4 | 40,000 | 0.03% |

| Investment Advisors/Asset Managers/Funds and others | 611.3 | 47.3 | 662.0 | ~185,500 | 0.36% |

| Total (USD Billion) | 842.5 | 68.5 | 917.5 | ~300,000 | 0.28% |

Source: NSDL FPI Monitor Data as of December 2024 ; USD/INR @84.5 and Quantum Advisors Estimates for Global AuM ~300 trillion; AuM assumed for: SWF – USD 13 trillion (globalswf.com); Pension Funds – USD 60 trillion (thinking ahead institute); Endowments and Foundations – USD 1.5 trillion ( US endowment survey and cfa institute); Insurance companies – USD 40 trillion (global insurance market report, 2024); Asset Managers – USD 145 trillion (PWC) and others are unaccountable and assumed at USD ~185 trillion; Total Global AuM is thus assumed at ~USD 300 trillion

Even if we assume that all investors have home bias and only a third of their assets are available to be invested globally, investments in Indian public equities (~USD 840 as of December 2024) is less than 1% of global investable AuM of US $ 100 trillion.

India’s weight in MSCI ACWI of ~2% is a lagging indicator of opportunity.

Investors are missing out on India’s returns by under-allocating following rigid ‘MSCI benchmarks’

(Source: GDP and Market Cap chart is from IMF and Bloomberg;(Source: India’s relative weighting chart in MSCI EM and MSCI ACWI Index is from a MSCI blog post of January 202312); As of December 2024, India’s weight in MSCI ACWI world is 1.9% as derived from iShares MSCI ACWI ETF)

However, as the above tables and chart suggest, global allocators remain bound by ‘MSCI guided weights’ for their allocation and rarely exceed that level. Also, they are wary of having single country allocations to countries like India, but do have large allocations to USA.

The under-allocation is despite Indian public equities being amongst the best asset large classes in the world to invest

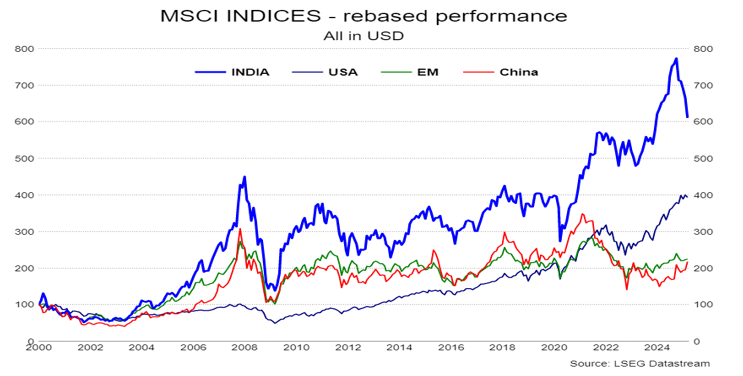

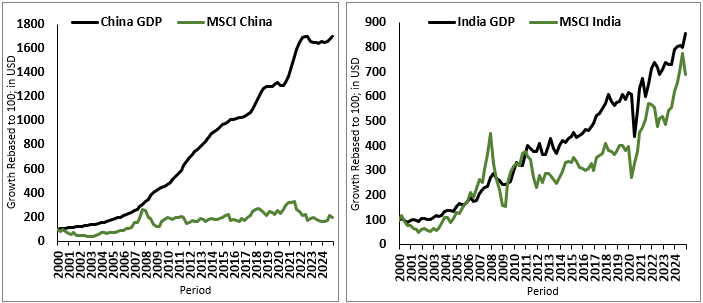

India GDP Growth is reflected in Equity Markets; making it easier to make a GDP weighted allocation of 5% to India

(Source: Bloomberg and MSCI, All data in USD, Quarterly Data till 31-December2024, Y-Axis Rebased to 100 on 31-Dec-1999. This is only for representation and understanding purpose and does not assure any promise or guarantee of same in the future. Past performance does not guarantee and is not indicative of future results.)

What if global investors allocate 5% of their portfolio to India

| What would 5% allocation to India mean for Investors | 2024 | 2034 E |

|---|---|---|

| India GDP in US $ Trillion % share of Global GDP |

USD 3.8 Tn ~3.5% |

USD 10 Tn ~5.8% |

| India Stock Market-Cap in US $ Trillion % share of Global M-cap |

USD 4.8 Tn ~4.0% |

USD 15 Tn ~6.5% |

| Of which - Foreign Investment in India US $ Trillion (Public + Private) % share of Available Global AUM (Estimated at USD 100 trillion – 1/3rd of total AUM) |

~USD 2.0 Tn* ~2.0% |

USD 5.0 Tn ~5% |

Source: Bloomberg Finance L.P; Quantum Advisors Estimates; Global AuM investable outside of the home country is estimated as USD 100 trillion out of a total estimated Global AuM of ~300 trillion; ) (* - We estimate market value of all foreign investment in India public investments at ~USD 900 billion (public equity (USD 840 bn, fixed income (50 bn) and alternative private assets at USD 1.0 trillon for the total to be USD 2.0 trillion); World and India GDP data is from IMF. World and India Market Cap data is from Bloomberg Finance L.P; Global Nominal GDP estimated to grow at 4.5%; Global market cap estimated to grow at 6%; India Nominal GDP estimated to grow at 10%; India market cap estimated to grow at 12%

An incremental 0.4% allocation (US$400 billion) to India every year from an investable global AuM of US$ 100 trillion over the next 5 years, is all it would take for global investors to have a meaningful allocation to India and participate in the long-term India opportunity.

Source Notes

-

Source: Economic Times

-

Source: Wikipedia article on US confiscating Japanese assets

-

Source: Federal Reserve History

-

Source: Pension and Investments online article on US share of global private capital

-

Source: IMF India Profile Page

-

Source: CEIC India Market Capitalisation

-

Source: MSCI Blog post on India Equity Futures for the World

Annexure: India was a large part of the global economy; India will be a large part of the global economy and deserves a higher weightage in global portfolios

(Source: Quantum Advisors; Angus Maddison, University of Groningen; Madison Project Database)

Ajit’s article February 9, 1990 in the Asian Wall Street Journal

The views expressed herein constitute only the opinions and do not constitute any guidelines or recommendation on any course of action to be followed by the reader

Important Disclosures & Disclaimers

The views expressed herein shall constitute only the opinions and any information contained in this material shall not be deemed to constitute an advice or an offer to sell/purchase or as an invitation or solicitation to invest in any security and further Quantum Advisors Private Limited (QAPL) and its employees/directors shall not be liable for any direct or indirect loss, damage, liability whatsoever arising from the use of this information.

Information sourced from third parties cannot be guaranteed or was not independently verified. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and the views given are fair and reasonable as on date. All the forward-looking statements made in this communication are inherently uncertain and we cannot assure the reader that the results or developments anticipated will be realized or even if realized, will have the expected consequences to or effects on, us or our business prospects, financial condition or results of operations.

Recipients should exercise due care and caution and if necessary, obtain the professional advice prior to taking any decision based on this information.

Important Notice:

This newsletter contains hyperlinks to websites operated by third parties. These linked websites are not under the control of QAPL and are provided for your convenience only. Clicking on those links or enabling those connections may allow third parties to collect or share data about you. When you click on these links, we encourage you to read the privacy notice of the website you visit. QAPL does not endorse, or guarantee products, services or advice offered by these websites.

UK related important disclosures:

• The content of this newsletter has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 (“FSMA 2000”). Reliance on this newsletter for the purpose of engaging in any investment activity may expose you to a significant risk of losing all of the property or other assets you invest or of incurring additional liability. This newsletter is exempt from section 21 FSMA 2000 on the grounds that it is directed only to certified sophisticated investors, high net worth companies, unincorporated associations, trusts and/or investment professionals within the meaning of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (“FPO”). The investment activity described in this newsletter is only available to these persons or entities and no other person or entity should rely on the contents of this document.

• The protections conferred by or under the Financial Services and Markets Act (FSMA) will not apply to this newsletter and any investment activity that may be engaged in as a result of this newsletter.

The applicability of any dispute resolution scheme or compensation scheme and its jurisdiction (if and where applicable) pertaining to a transaction resulting from this newsletter would be as specified in the respective client agreements.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.